The energy transition is no longer just about renewables vs. hydrocarbons it’s spawning entirely new niches where traditional oil & gas expertise is being repurposed. In 2026, search interest is exploding around three high-growth areas:

- Critical minerals migration (lithium drilling, rare earth mining) by integrated oil majors

- Small Modular Reactors (SMRs) as carbon-free power for industrial campuses

- Sustainable Aviation Fuel (SAF) refinery conversions

These niches represent diversification plays for IOCs, new power solutions for data centers & industry, and decarbonization mandates for aviation. Subsea and subsurface skills from offshore oil & gas are directly transferable.

1. Critical Minerals Migration: IOCs Pivot to Lithium & Rare EarthsIntegrated oil companies (IOCs) are rapidly entering the critical minerals space, leveraging their subsurface drilling, reservoir characterization, and project execution expertise.

Top search drivers in 2026:

- “lithium drilling ExxonMobil”

- “rare earth mining oil companies”

- “ExxonMobil lithium brine extraction”

Key moves:

- ExxonMobil : Leading the charge with its Lithium business unit. In 2026, Exxon is scaling direct lithium extraction (DLE) from brine formations in Arkansas (Smackover Formation) and is evaluating similar plays in the U.S. Gulf Coast and South America. They apply oilfield technologies: horizontal drilling, reservoir modeling, and produced water management.

- Chevron, Occidental, EOG : Exploring lithium in brine co-production from existing oil & gas fields, plus rare earth element (REE) recovery from produced water and drill cuttings.

- Subsurface synergy : HPHT drilling experience helps in deep brine formations; seismic interpretation maps lithium-rich zones; subsea tech adapts to offshore brine extraction pilots.

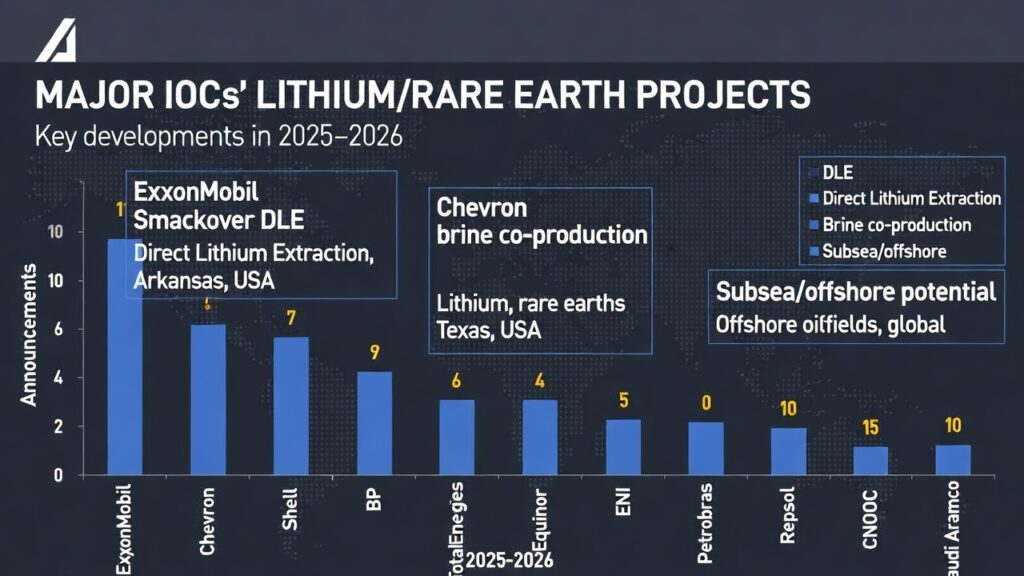

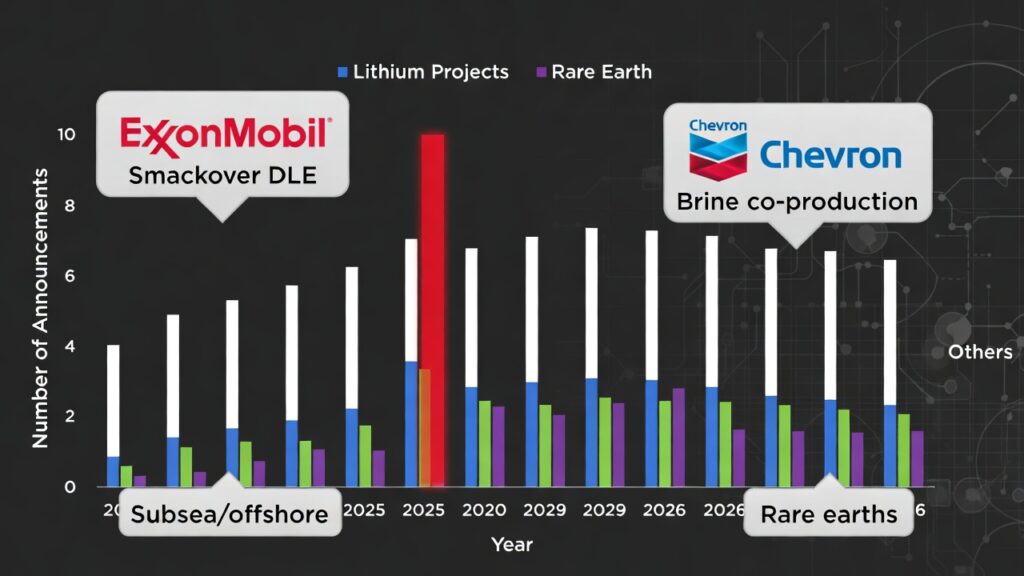

Figure 1: Critical Minerals Diversification by IOCs

( image: Bar chart showing lithium/rare earth project announcements by major IOCs in 2025–2026, with callouts for ExxonMobil Smackover DLE, Chevron brine co-production, and subsea/offshore potential.)

This trend is driven by EV battery demand and U.S./EU supply chain security IOCs are turning “waste” brine into high-value lithium carbonate.

2. Small Modular Reactors (SMRs): Carbon-Free Power for Energy-Intensive CampusesSMRs are trending as a reliable, carbon-free baseload solution for power-hungry industrial sites especially AI data centers, refineries, and offshore platforms.High-volume searches:

- “small modular reactors AI data centers”

- “SMR nuclear for industrial power 2026”

- “carbon-free power campus SMR”

Why SMRs are surging:

- 24/7 reliability — Unlike wind/solar, SMRs deliver constant output (50–300 MW per module).

- Compact footprint — Factory-built, transportable modules fit on existing industrial sites.

- Key players — NuScale, GE-Hitachi (BWRX-300), TerraPower (Natrium), X-energy (Xe-100) are targeting first deployments 2028–2030.

- Use cases — Microsoft, Google, Amazon exploring SMRs for data-center campuses. Offshore platforms and LNG terminals are evaluating floating SMR concepts for self-power + export.

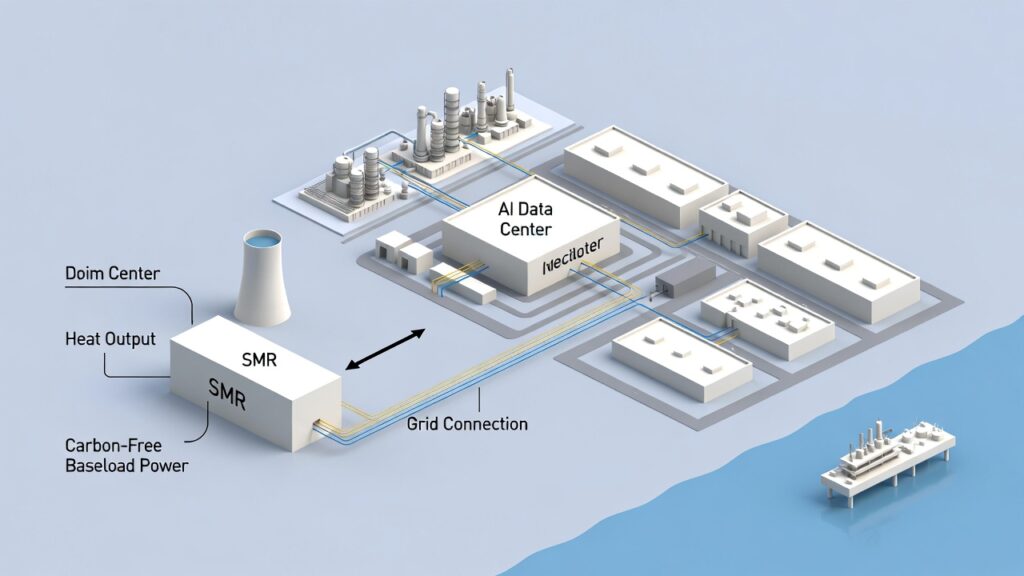

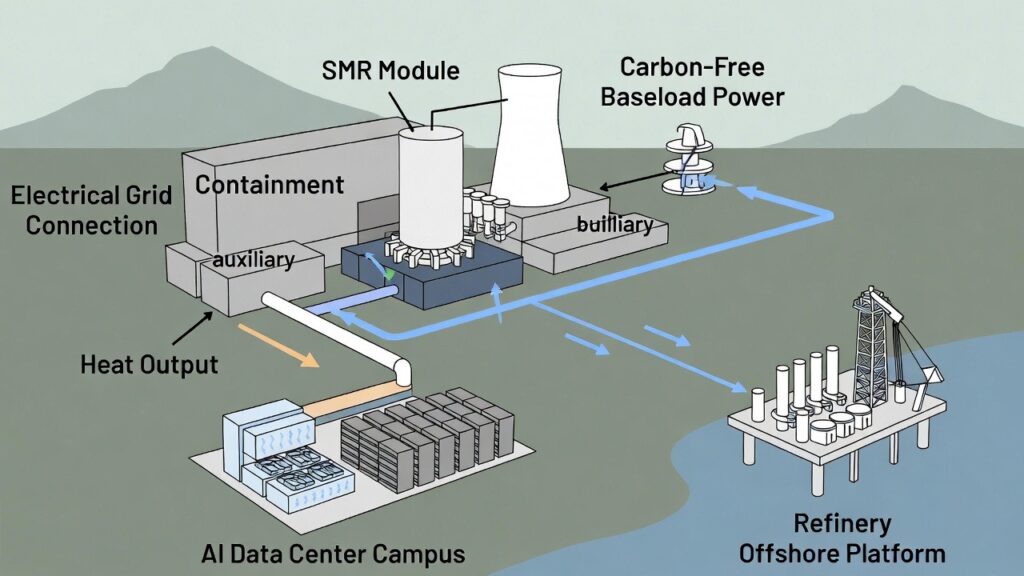

Figure 2: SMR Power for Industrial Campuses

( image: Conceptual schematic showing SMR module powering AI data center campus, refinery, or offshore platform, with labels for heat output, grid connection, and carbon-free baseload.)

SMRs bridge the gap until renewables + storage scale to GW levels making them a hot topic for energy-intensive users.

3. Sustainable Aviation Fuel (SAF): Refinery Conversion & Feedstock ChallengesAs global aviation regulations tighten (EU ReFuelEU, U.S. SAF Grand Challenge), searches for “refinery conversion for SAF”, “SAF production 2026”, and “sustainable aviation fuel refinery” are trending among investors and operators.

Key trends:

- Refinery retrofits : Existing crude refineries are converting units to produce SAF via HEFA (hydro processed esters and fatty acids) or Fischer-Tropsch pathways. Examples: Phillips 66 Rodeo Renewed (California), Marathon Martinez (California), and multiple Gulf Coast projects.

- Feedstock : Waste oils, fats, greases, and emerging bio-crudes from algae or municipal waste. Oil majors are leveraging refining expertise.

- Subsea tie-in : Future SAF projects may use offshore bio-feedstock platforms (algae farms) with subsea export lines.

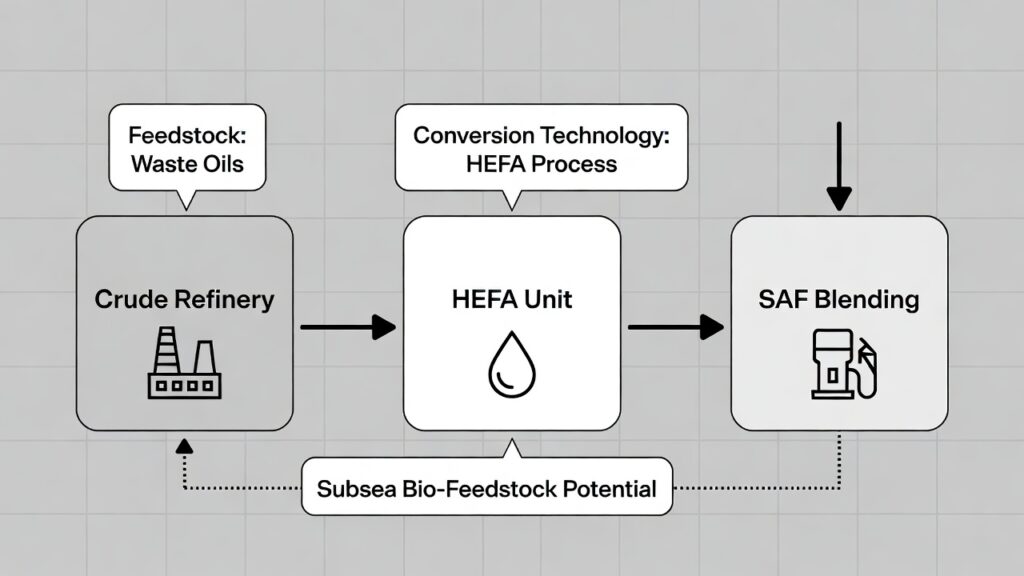

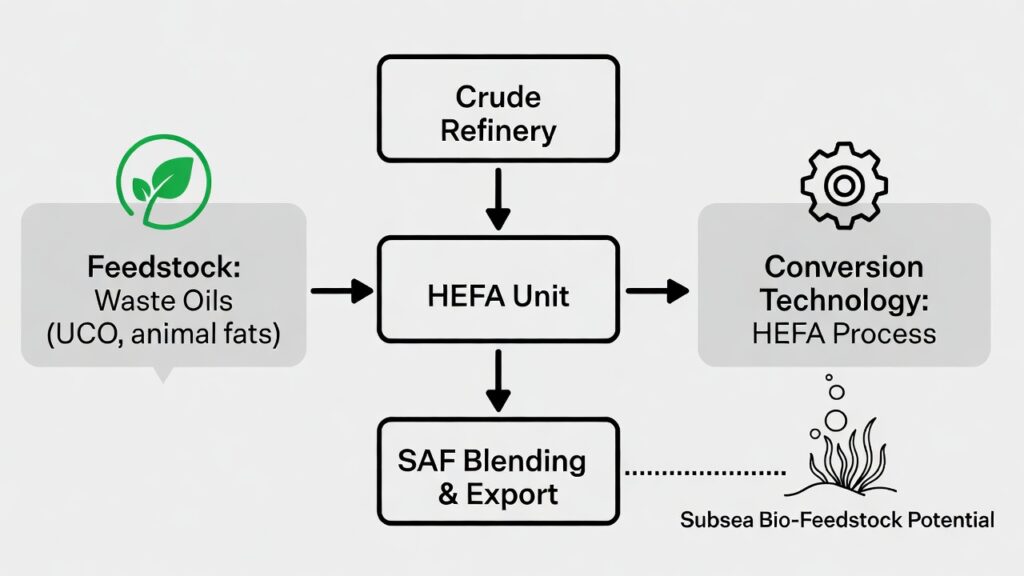

Figure 3: SAF Refinery Conversion Pathways

( image: Flow diagram showing crude refinery → HEFA unit → SAF blending → export to airports, with callouts for feedstock (waste oils), conversion tech, and subsea bio-feedstock potential.)

SAF is one of the few aviation decarbonization options with scale potential driving refinery investment and feedstock innovation.

The Bottom Line for 2026

The energy transition is creating emerging niches where oil & gas expertise is highly valuable:

- Critical minerals : IOCs like ExxonMobil apply drilling/reservoir skills to lithium & rare earths.

- SMRs : Carbon-free base load for AI/industrial campuses.

- SAF : Refinery conversions and feedstock supply chains.

Subsea and subsurface technologies (drilling, pipelines, monitoring) are directly transferable positioning offshore specialists at the center of these growth areas.Engineers and investors: Which niche excites you most lithium brine extraction, SMRs for data centers, or SAF refinery retrofits?

Drop a comment or connect on LinkedIn. The future is diversified and subsea is everywhere.

Oko Immanuel

Subsea Engineering Specialist | Offshore Pipeline Insight