By Oko Immanuel, M.Eng – Founder, Offshore Pipeline Insight

March 22, 2026

Shell remains the world’s largest integrated LNG player, with a massive trading portfolio (~100 MTPA) and upstream assets across the globe. In 2026, Shell is focusing on LNG growth as a reliable, lower-carbon backbone fuel, while scaling back some renewables to prioritize upstream cash flow. Subsea technology is central to Shell’s LNG feed-gas supply, with HPHT flow lines, manifolds, and subsea compression supporting key projects.

Key Shell LNG Projects & Subsea Infrastructure in 2026

- Qatar North Field Expansion (NFE & NFS)

- Shell stake: 6.25% in NFE (QatarEnergy LNG), similar in NFS.

- Capacity: NFE adds 32–33 MTPA (first trains 2026); NFS adds 16 MTPA (2027–2028).

- Subsea focus: Shell contributes expertise in subsea tiebacks and flow assurance for the ~500 km pipeline network (trunk + intra-field) feeding Ras Laffan. HPHT-rated subsea trees, manifolds, and PIP sections manage high-pressure sour gas. Digital twins and fiber-optic monitoring ensure integrity.

- LNG Canada (Kitimat, BC)

- Shell stake: 40% (joint venture with Petronas, PetroChina, Mitsubishi, KOGAS).

- Status: First cargo shipped June 2025; full ramp-up 2026.

- Subsea role: Feed-gas from offshore fields via subsea pipelines and onshore processing. Shell’s Prelude FLNG experience informs flow assurance and compression.

- Prelude FLNG (Australia)

- Status: Operational, backfill from Crux field (startup 2026–2027).

- Subsea focus: Extensive subsea infrastructure (flowlines, manifolds, risers) to FLNG vessel. Dynamic risers and mooring systems handle remote, deepwater conditions.

- Nigeria LNG (NLNG) Train 7

- Shell stake: 25.6%.

- Status: Under construction, startup 2026–2027.

- Subsea tie-in: HI offshore gas project (Shell FID 2025) supplies 350 MMscfd via subsea pipelines to Bonny Island terminal.

- Other active projects

- NLNG T7 backfill — Manatee and Aphrodite fields (Trinidad & Tobago) via subsea tiebacks.

- Gorgon Jansz Compression Subsea compression to maintain gas supply (startup 2028+).

Figure 1: Shell Global LNG Portfolio Map

( image: World map highlighting Shell’s key LNG supply sources (Qatar NFE/NFS, Australia Prelude/Crux, Nigeria NLNG, LNG Canada), with subsea pipeline/callout icons for HPHT flowlines, manifolds, and compression.)Shell’s LNG strategy emphasizes reliable supply, competitive pricing, and sustainability (methane abatement + CCS) — solving the energy trilemma.

Chevron Energy Trends in 2026

Chevron (NYSE: CVX) is executing a disciplined, upstream-focused strategy in 2026, with heavy investment in oil & gas growth while advancing lower-carbon initiatives. Capex guidance of $18–19B (potentially up to $21B) prioritizes high-return upstream, with subsea tech playing a key role in deepwater and LNG feed-gas.

Chevron 2026 Energy Trends & Subsea Focus

- Upstream Growth

- Capex: ~$17B total upstream, with $10.5B in U.S. (Permian, DJ, Bakken shale; GoM deepwater).

- Production target: >2 MMboed in U.S. alone.

- Subsea role: GoM deepwater tiebacks (Anchor, Kaskida follow-ons) use HPHT subsea trees, flowlines, and manifolds. Subsea boosting/compression maintains flow from distant fields.

- LNG & Gas

- Gorgon (Australia) World’s largest CCS at an LNG facility (up to 4 Mtpa CO₂ injection).

- Gorgon Stage 3 — FID 2025, subsea tiebacks from Geryon/Eurytion fields to Barrow Island. Subsea gas gathering system (largest in Australia) expanded with compression.

- Subsea tech: Subsea pipelines, manifolds, injection trees for CCS; fiber-optic monitoring for integrity.

- Lower-Carbon & CCS

- $1B allocation Reducing carbon intensity + new energies (CCS, hydrogen).

- Bayou Bend CCS (Texas) One of largest planned CO₂ storage hubs.

- Subsea focus: Evaluating subsea injection in GoM depleted reservoirs; subsea pipelines for CO₂ transport.

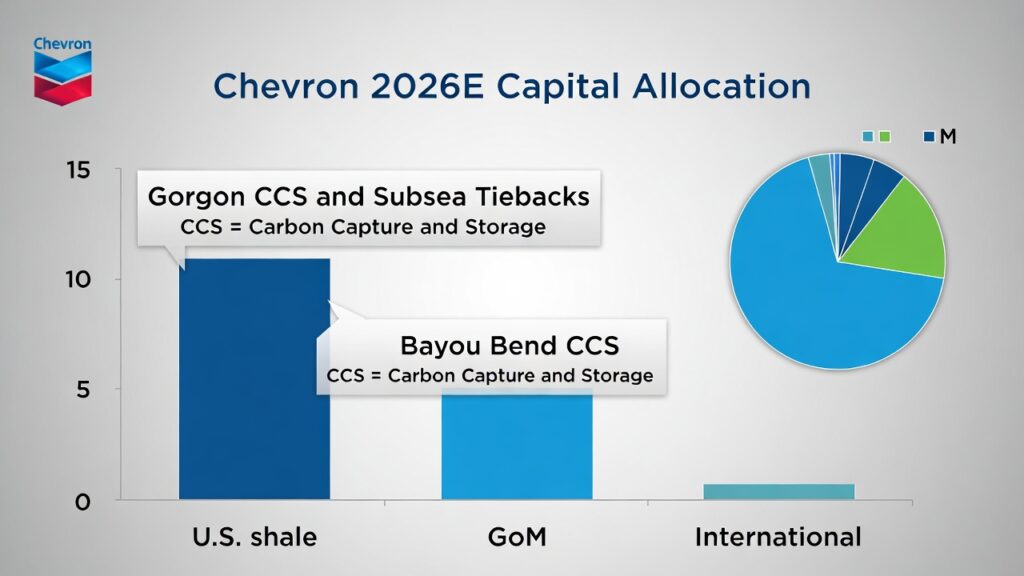

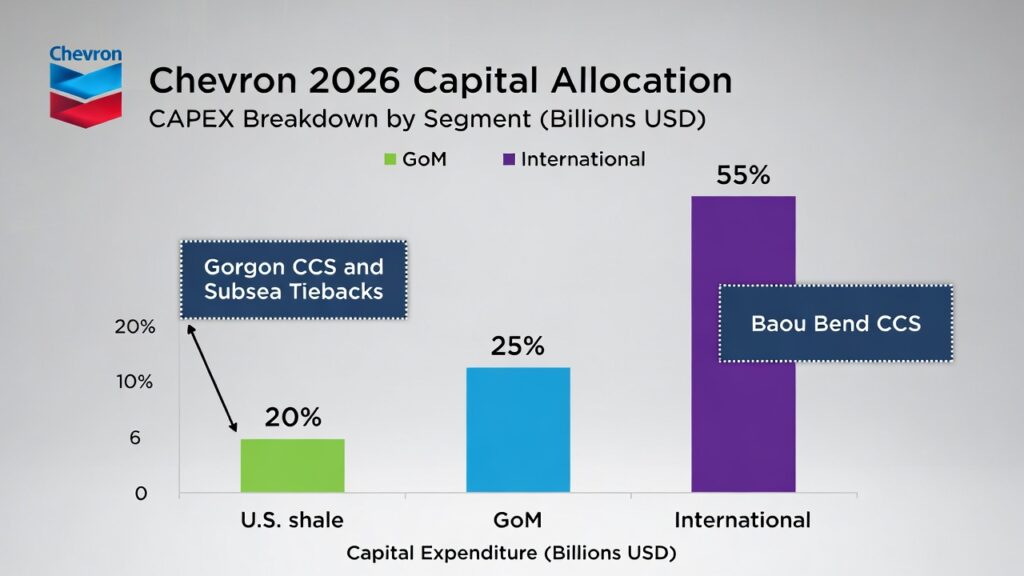

Figure 2: Chevron 2026 Capex Allocation & Subsea Focus

( image: Pie/bar chart showing upstream capex breakdown (U.S. shale, GoM, international), with callouts for Gorgon CCS/subsea tiebacks and Bayou Bend CCS.)

Chevron’s 2026 trend is clear: upstream strength funds transition (CCS, hydrogen), with subsea tech enabling reliable, low-carbon LNG and gas supply.Engineers: Which subsea tech is most critical for LNG/CCS — HPHT pipelines, subsea compression, or monitoring?

Comment below .

Shell & Chevron are proving balance wins.

Oko Immanuel

Subsea Engineering Specialist | Offshore Pipeline Insight