Pivot from Broad Decarbonization to Methane Abatement

By Oko , M.Eng | Offshore Pipeline Insight | June 2026

After years of heavy investment announcements in renewables, many upstream operators are quietly recalibrating. Broad diversification into solar, wind, and other green ventures is being deprioritized in favor of laser-focused operational decarbonization — especially aggressive methane abatement and leak detection.

This pragmatic pivot delivers fast, measurable emissions cuts, strong financial returns, and compliance with tightening global regulations.Methane (CH₄) is over 80 times more potent than CO₂ over a 20-year period. Reducing it offers one of the highest-impact, lowest-cost levers available to the oil and gas sector today.

Why the Strategic Pivot Is Happening Now

Many majors and independents found that large-scale renewable investments often delivered lower returns, higher execution risks, and limited near-term emissions impact compared to fixing their own operations. Methane abatement, by contrast, frequently pays for itself through captured gas sales while directly addressing a potent climate forcer.

Key Drivers in 2026:

- Regulatory Pressure: Europe’s Methane Regulation and CBAM (fully effective from 2026) demand strict monitoring, reporting, and verification (MRV) for both domestic and imported oil/gas.

- Investor & Market Demands: Buyers (especially in Europe) increasingly require low-methane-intensity supply.

- Economic Reality: 30–50% of methane abatement options cost nothing or generate positive returns via avoided product loss.

- Satellite & Tech Maturity: Continuous monitoring via drones, satellites, and sensors makes leaks detectable and fixable in near real-time.

Blick auf die von TAQA betriebene, Cormorant A (Alpha) Ölplattform im britischen Teil der Nordsee im Cormorant Ölfeld.

Caption: Offshore platform with visible flaring — a key target for methane abatement campaigns in 2026.

Understanding Methane Sources in Oil & Gas

Upstream operations account for ~80% of oil and gas sector methane emissions. Primary sources include:

- Fugitive leaks from valves, flanges, compressors, and pipelines.

- Venting during maintenance or pressure relief.

- Incomplete combustion from flares.

- Unintended releases from storage tanks and wellheads.

The IEA estimates that over 50 Mt of annual upstream methane could be abated with existing technologies, with nearly 30 Mt at no net cost.

Technologies Driving Methane Abatement in 2026

Operators are deploying a multi-layered approach:

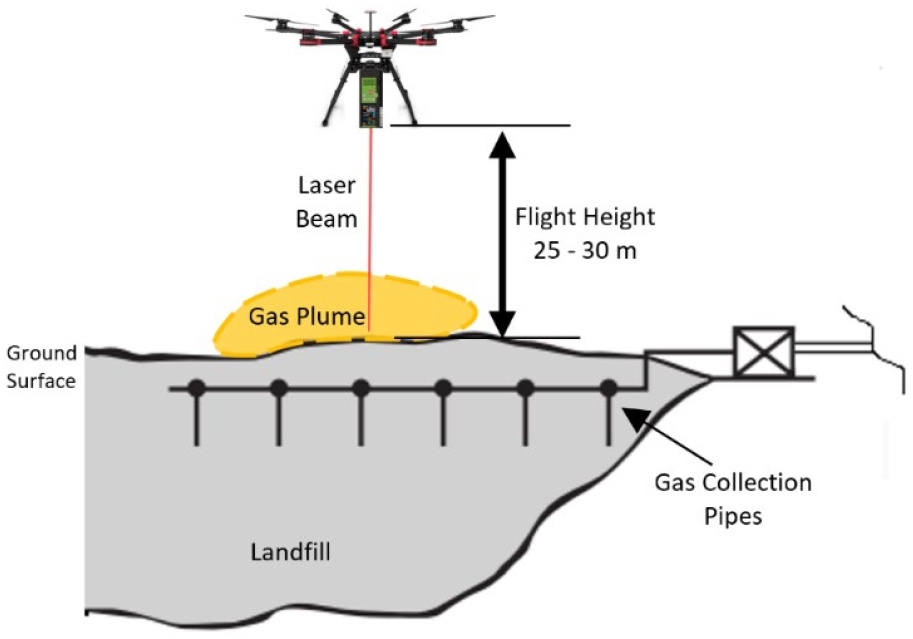

- Continuous Monitoring — Fixed IoT sensors, optical gas imaging (OGI) cameras, and drone fleets.

- Satellite Detection — Public and commercial satellites (e.g., MethaneSAT, GHGSat) identify super-emitters.

- Leak Detection & Repair (LDAR) — Moving from annual to quarterly or continuous programs.

- Flaring & Venting Reduction — Vapor recovery units (VRUs), microturbines, and reinjection.

- Equipment Upgrades — Zero-emission pneumatic controllers and electric pumps.

Offshore-Specific Solutions:

- AUVs/ROVs with methane sensors for subsea infrastructure.

- Floating platform retrofits for flare minimization.

- Integration with existing subsea tiebacks and umbilicals for chemical injection and monitoring.

Caption: Advanced monitoring on offshore assets — combining drones, sensors, and satellite data for comprehensive methane management.

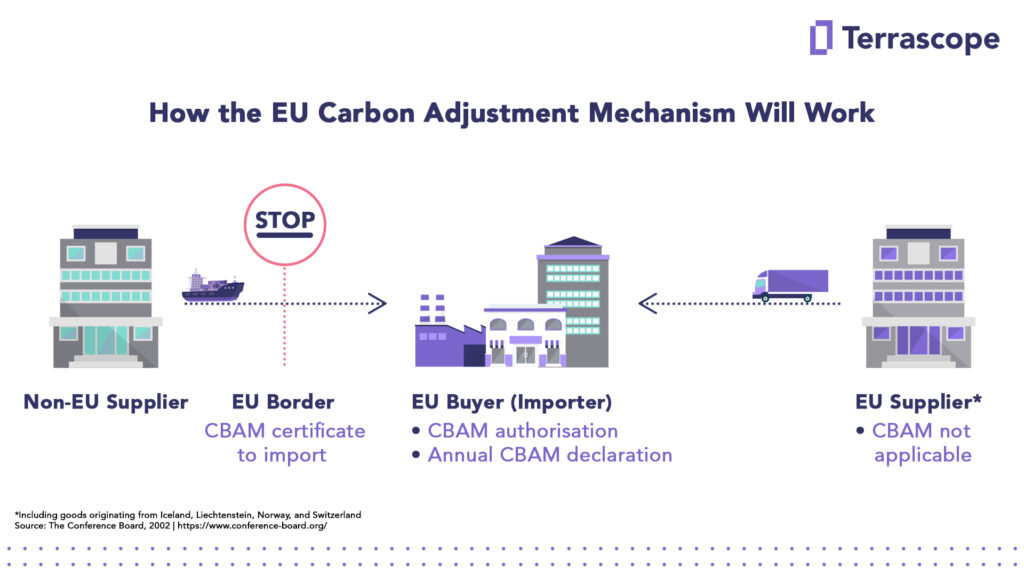

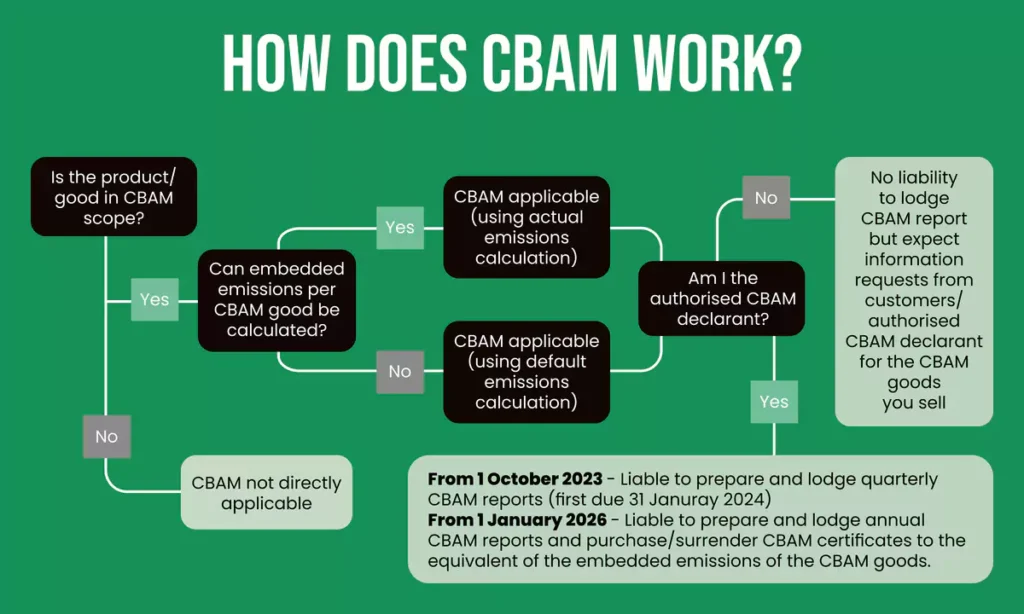

Regulatory Pressure: Europe’s CBAM and Methane RulesThe EU’s Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase in 2026, putting a price on embedded emissions in imported goods. While methane itself is not directly covered under CBAM certificates (which focus on CO₂), the separate EU Methane Regulation requires:

- Strict MRV standards for all oil, gas, and coal imports.

- Leak detection campaigns and repair timelines.

- Phased methane intensity limits starting 2030.

- Transparency database launch in September 2026.

Non-compliant suppliers risk losing access to the lucrative EU market. This has accelerated global adoption of OGMP 2.0 standards.

Caption: How the EU CBAM and Methane Regulation create strong incentives for low-methane supply chains.

Case Studies: Majors Shifting Focus

- ExxonMobil: Targeting 70–80% methane intensity reduction by end-2026 with continuous monitoring rollouts.

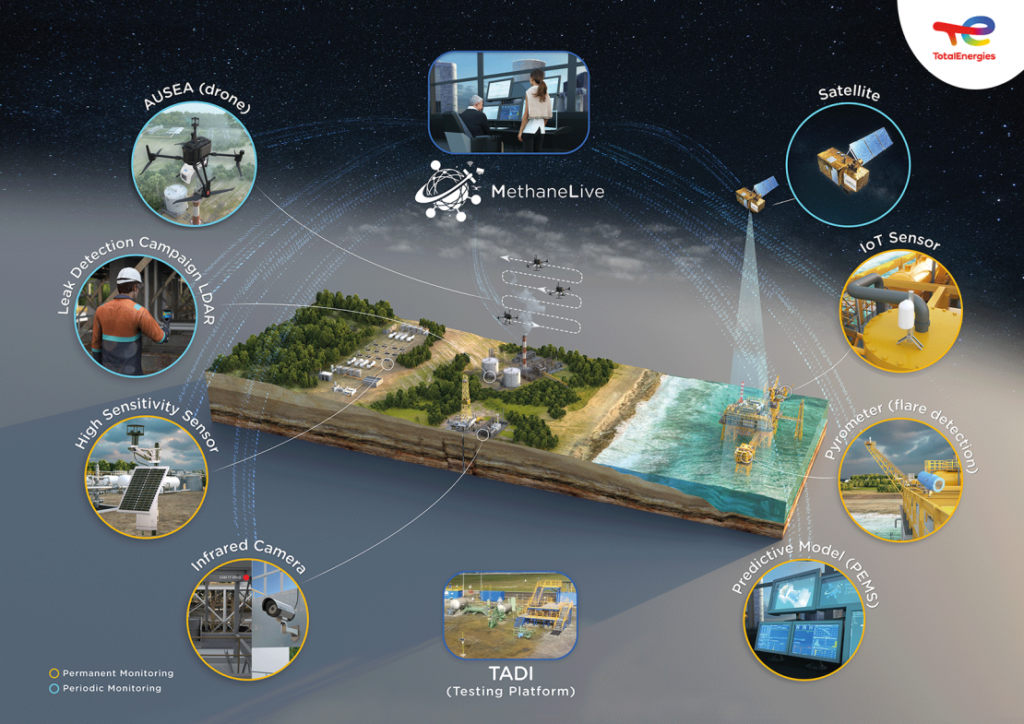

- TotalEnergies: Deploying AUSEA drones, satellites, and MethaneLive platform across operated assets.

- Shell & BP: Prioritizing OGMP 2.0 Level 5 (gold standard) reporting and ending routine flaring.

Many operators report that methane projects deliver faster ROI than many renewable ventures.

Implications for Offshore Pipeline & Subsea Professionals

This strategic shift creates strong demand for:

- Advanced pipeline integrity monitoring (fiber-optic, acoustic sensors).

- Methane-ready materials and leak-tight designs for new tiebacks.

- Integration of continuous emission sensors into umbilicals and subsea systems.

- Retrofit opportunities on existing flowlines and risers.

- CCUS and hydrogen blending projects that require ultra-low fugitive emissions.

Pipeline professionals are at the center of this transition — designing, maintaining, and monitoring the infrastructure that must demonstrate near-zero methane intensity.

The Pragmatic Path Forward

The industry is not abandoning the energy transition — it is prioritizing the highest-impact, lowest-cost actions first. Methane abatement delivers immediate climate benefits, improves operational efficiency, generates revenue from saved gas, and ensures regulatory compliance in a fragmenting global market.

Broad renewable diversification will continue selectively, but operational excellence in methane reduction has become the new baseline expectation for credible operators.

What methane abatement technologies or projects are you seeing in your operations? Share your experiences with LDAR, satellite monitoring, or regulatory compliance in the comments — especially offshore and pipeline professionals.

Next in the series: Hybrid Energy Hubs — Combining Gas, Wind, and Hydrogen.Sources: IEA Global Methane Tracker 2026, EU Methane Regulation, OGMP 2.0, company reports (ExxonMobil, TotalEnergies, etc.), 2025–mid-2026 data.