By Oko Immanuel, MSc in Subsea Engineering.

Published: May 06, 2026I

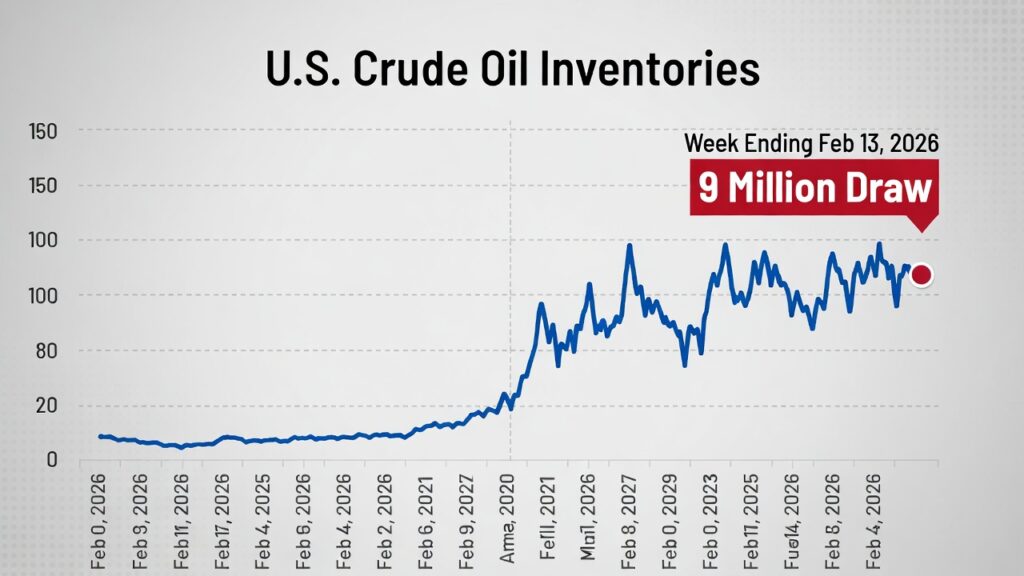

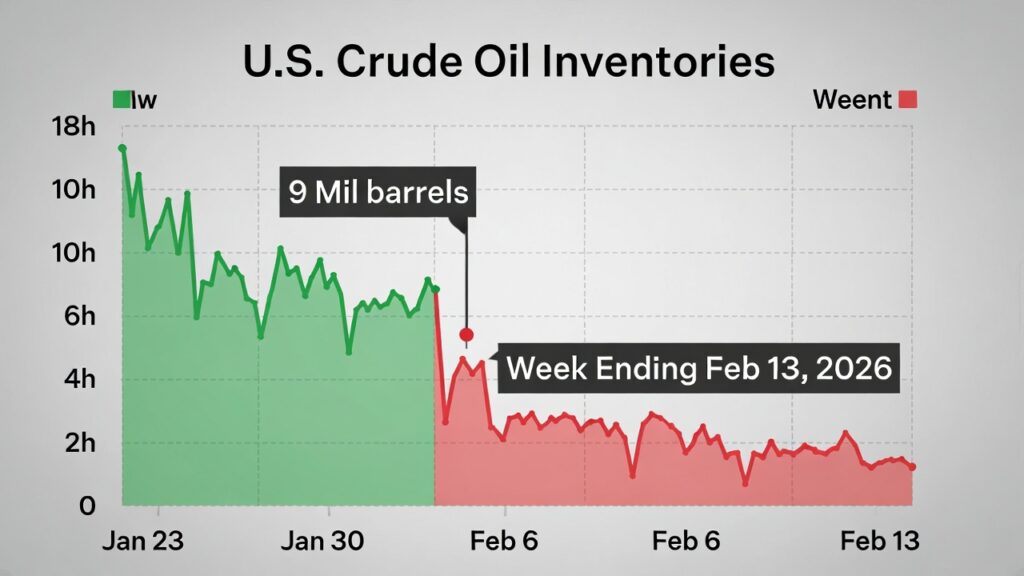

In a surprise move that caught many analysts off guard, U.S. crude oil inventories fell sharply by 9 million barrels last week (week ending February 13, 2026), according to the latest EIA Weekly Petroleum Status Report released today. This brings commercial stockpiles down to 419.8 million barrels—about 5% below the five-year seasonal average. The draw was the largest in five months and far exceeded expectations of a modest build (around +2.1 million barrels in Reuters polls).

The plunge contributed to today’s oil price rally, with Brent crude climbing to around $71+ per barrel and WTI nearing $66+, building on earlier geopolitical-driven gains. Here’s a quick look at the data and its ripple effects on offshore projects.

(Chart showing recent U.S. crude inventory changes, highlighting the massive 9 million barrel draw in the week to February 13, 2026.)

Key Highlights from the EIA Report

- Crude draw: -9 million barrels (to 419.8 mbbl), with Cushing (WTI delivery hub) down -1.1 million barrels.

- Gasoline stocks: -3.2 million barrels (to 255.8 mbbl), first decline in 14 weeks.

- Distillate stocks (diesel/heating oil): -4.6 million barrels.

- Refinery activity: Inputs rose +77,000 b/d to 16.1 million b/d; utilization hit 91.0%.

- Imports fell -281,000 b/d to 6.5 million b/d, while exports and demand strengthened.

The unexpected tightness stems from higher refinery runs (processing more crude into fuels) amid rising U.S. consumption and lower imports creating a bullish supply signal.

Implications for Offshore Projects

For offshore and subsea developments (especially HPHT and deepwater tiebacks), this inventory draw reinforces a supportive price environment:

- Economics boost: Sustained $70+ oil prices improve breakevens for capital-intensive HPHT projects. Operators gain confidence for final investment decisions (FID) on delayed fields, where high costs (thick-walled pipes, CRAs, advanced insulation) require stronger margins.

- Demand signal: Stronger refinery throughput and product draws indicate healthy downstream demand, which could spur more offshore production to meet future needs particularly in gas-rich regions like the Gulf of Mexico or Guyana.

- Supply chain & integrity focus: Tighter inventories may accelerate drilling and tiebacks, increasing demand for reliable subsea systems. Flow assurance (preventing hydrates/wax in longer lines) and integrity management (corrosion monitoring, digital twins) become even more critical to avoid downtime in a high-price market.

However, volatility remains: Geopolitical risks (US-Iran tensions) and OPEC+ decisions could cap or amplify the rally. For engineers, this is a reminder to prioritize resilient designs controlled buckling, robust cathodic protection, and predictive tools—to deliver projects on time and budget.

This EIA draw is a classic bullish indicator: lower stocks + rising demand upward pressure on prices. For offshore pipeline and subsea pros, it highlights the ongoing need for efficient, low-risk developments to capitalize on stronger fundamentals.

What do you think will this inventory tightness sustain the rally, or is it a short-term blip?

Share your take in the comments!Share on LinkedIn or X for energy colleagues.

Subscribe for more HPHT, flow assurance, integrity insights, and weekly energy updates. Subsea Opportunities in the Caribbean.)