By Oko Immanuel, M.Eng in Subsea Engineering

Published: May 06 , 2026

As we wrap up the week, the oil and gas sector is buzzing with geopolitical risk premiums, upward price momentum, and fresh US offshore leasing signals. Here’s the key trending news from today (February 20, 2026) that matters for offshore, HPHT, subsea, and energy professionals.

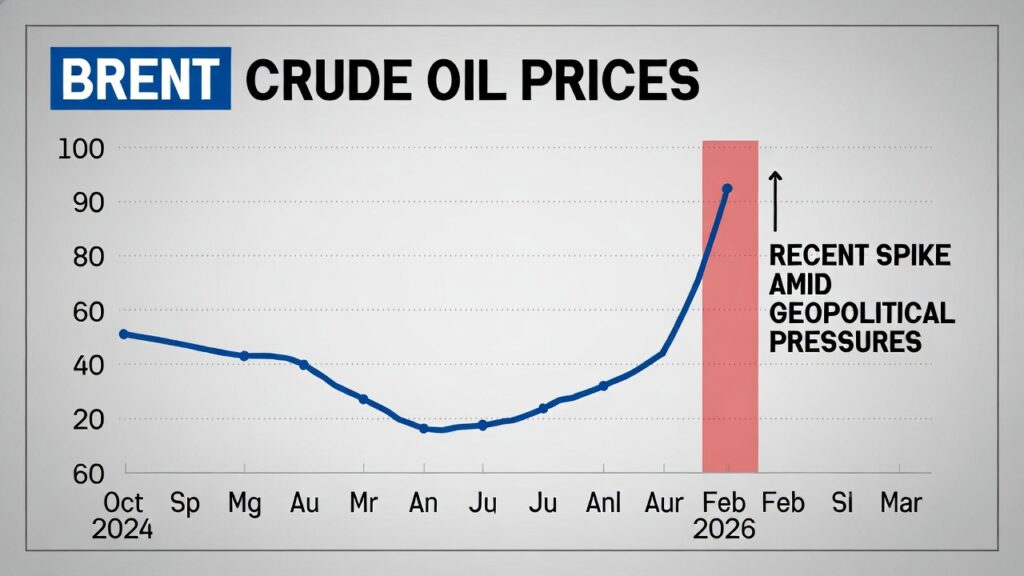

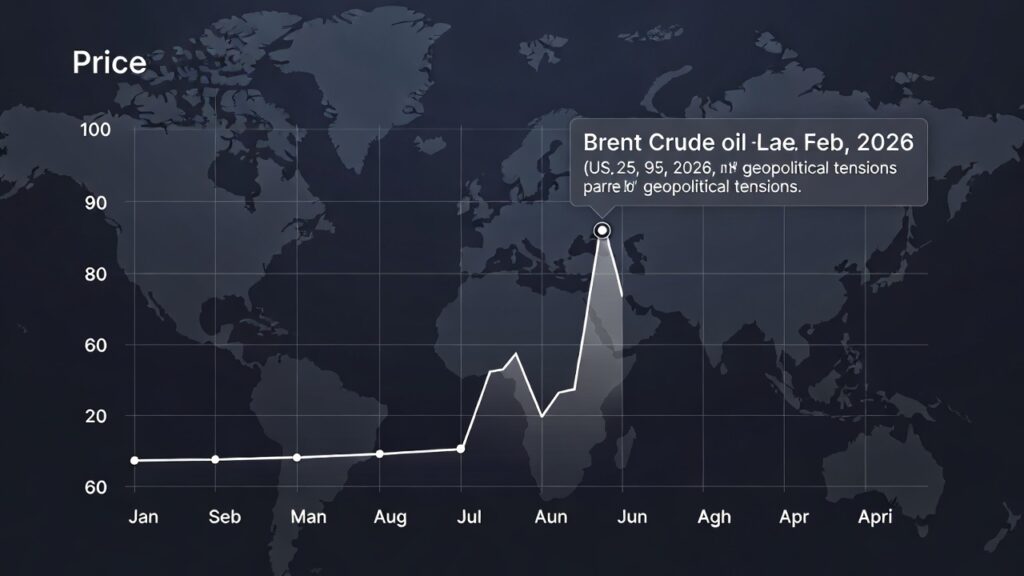

1. Oil Prices Push Toward Weekly Gains on US-Iran TensionsBrent crude futures rose modestly today to around $71.91–$72.13 per barrel (up 0.4–0.6%), while WTI climbed to $66.62–$66.84 (up 0.4–0.7%). This keeps both benchmarks at six-month highs (highest since late July/August 2025) and on track for their first weekly gain in three weeks (roughly +5–6% so far).

The catalyst remains escalating US-Iran standoff: President Trump set a 10–15 day deadline for Tehran to reach a nuclear deal, with warnings of “really bad things” if no agreement. Reports of US military buildup, Iran’s planned joint naval drills with Russia in the Sea of Oman, and temporary Strait of Hormuz closures during exercises are fueling fears of supply disruptions. The Strait handles ~20–30% of global seaborne oil—any threat could push prices to $90–$100+, analysts warn.

Offshore tie-in: Higher prices support HPHT/deepwater project economics (better breakevens for CAPEX-heavy designs like CRAs, induction-heated joints, and digital twins). But supply chain risks rise—insurance premiums, rerouting delays, and integrity threats in volatile regions.

(Brent crude price trend chart showing the recent spike amid geopolitical pressures in February 2026.)

2. BOEM Proposes Third Gulf of Mexico Lease Sale for August 2026The Bureau of Ocean Energy Management (BOEM) published the Proposed Notice of Sale for Big Beautiful Gulf 3 (BBG3) today, scheduling the third offshore oil & gas lease sale under the One Big Beautiful Bill Act for August 12, 2026. This starts a 60-day public comment period.Following BBG2 (slated for March), this sale continues the push for expanded US Gulf leasing—offering millions of acres across Western, Central, and Eastern planning areas (water depths 9 ft to >11,100 ft). It’s part of a mandated series of 30 Gulf sales to boost domestic production and energy security.Relevance for subsea/HPHT: More blocks could accelerate deepwater tiebacks, increasing demand for advanced pipeline designs, flow assurance strategies (e.g., hydrate prevention in longer lines), and integrity monitoring tools.

3. Fitch: Oil Prices to Support Solid Middle East Growth in 2026Fitch Ratings forecasts 4% median economic growth across GCC countries, Egypt, Iraq, Israel, and Jordan in 2026 (up from 3.4% in 2025), driven by oil prices remaining above fiscal break-even levels for most GCC sovereigns despite softer markets overall. Public spending stays underpinned, positive for regional offshore investments (e.g., ADNOC expansions, Saudi Aramco projects).Implication: Sustained regional activity supports global subsea hardware demand and opportunities for HPHT innovations in Middle East waters.

Overall vibe: Short-term bullish on prices due to geopolitics, with US policy pushing domestic offshore growth. Offshore engineers should monitor Strait risks for supply chain integrity and leverage higher prices for project momentum.

What trending story excites (or concerns) you most this week? Drop a comment—let’s chat about how these developments impact HPHT designs, flow assurance, or subsea integrity!Share on LinkedIn/X for energy colleagues.

Subscribe for daily/weekly offshore insights, HPHT series updates, and free checklists.