By Oko Immanuel February 2 2026

Founder & Owner, Offshore Pipeline Insight

M.Eng in Subsea Engineering | Former Roughneck | Texas A&M Alumnus

The energy sector in 2026 is a tale of two markets: oil & gas navigating oversupply and disciplined capital, while gold surges as a safe-haven asset amid uncertainty. Both intersect with offshore infrastructure gold’s rally supports mining capex (including subsea pipelines for slurry transport), while oil & gas trends drive demand for HPHT pipelines, integrity monitoring, and transition repurposing.

1. Oil & Gas in 2026 – Supply Glut, LNG Strength, Capital Discipline

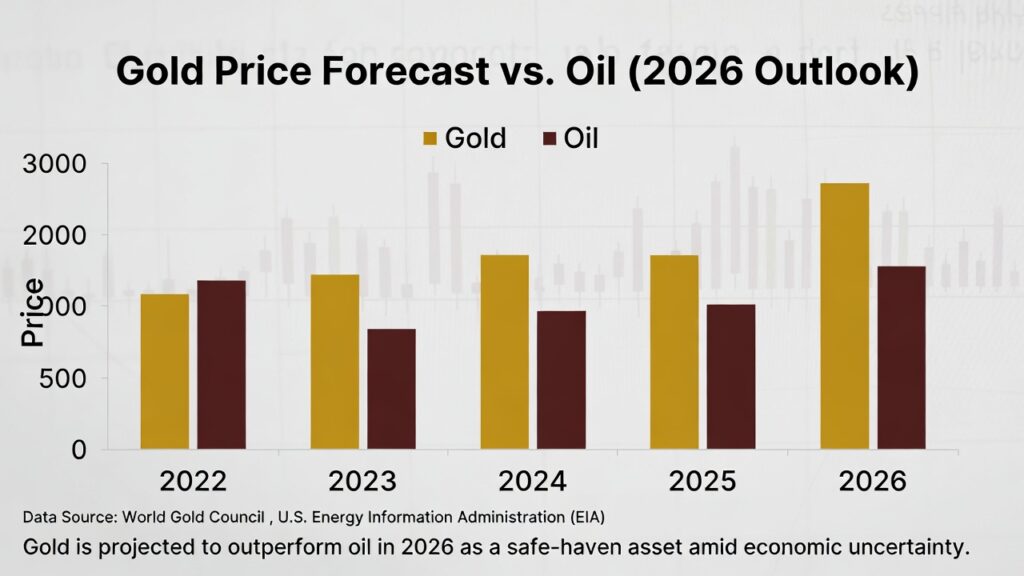

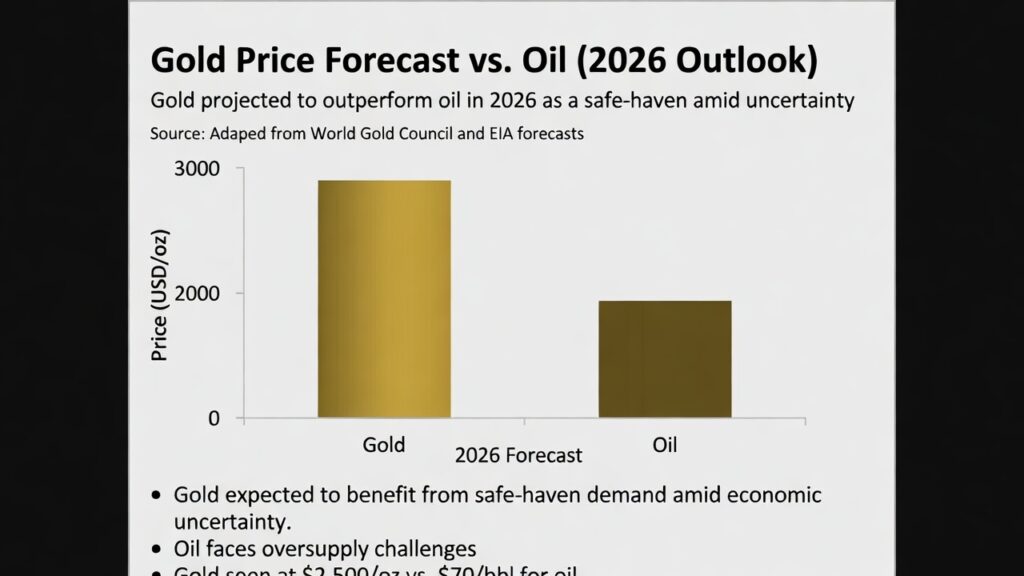

- Oil prices: Brent averaging $58–62/bbl (EIA & IEA consensus), down from 2025 due to non-OPEC growth (US, Guyana, Brazil) outpacing demand. Global supply surplus expected to reach 0.5–1 mb/d by mid-2026.

- Demand growth: Modest at 0.9–1.1 mb/d, held back by economic slowdowns and EV adoption.

- LNG boom: Global LNG supply up 7–9%, led by US (Plaquemines, Corpus Christi), Qatar (North Field East), and Canada. Spot prices volatile but Asia demand strong.

- Capital discipline: Majors prioritize free cash flow and shareholder returns over aggressive FIDs. Greenfield projects deferred; brownfield tiebacks and life extension dominate.

- Offshore implications: Deepwater & HPHT tiebacks remain active (Gulf of Mexico, North Sea, Brazil pre-salt). Subsea EPC steady, but operators demand cost efficiency.

Diagram: Gold Price Forecast vs. Oil (2026 Outlook)Gold vs Oil Price Forecast 2026

Gold projected to outperform oil in 2026 as a safe-haven amid uncertainty. Source: Adapted from World Gold Council & EIA forecasts.

2. Gold Market in 2026 – Safe-Haven Surge & Mining Impact

- Price forecast: Gold averaging $2,800–$3,200/oz (some analysts see $3,500+), driven by:

- Central bank buying (China, India, Turkey).

- Geopolitical risk (Middle East tensions, US policy shifts).

- Inflation hedge & declining real yields.

- Mining & infrastructure: Higher gold prices boost exploration and capex in remote/offshore-adjacent projects (e.g., deep-sea nodules, Arctic mining). Subsea pipelines for slurry transport (tailings, ore concentrate) see renewed interest in gold-rich regions (Papua New Guinea, Indonesia, Arctic Canada).

3. Intersection: Offshore Energy & Gold Rally

- Pipeline crossover: Gold mining often requires long-distance slurry pipelines (similar to HPHT oil/gas lines in design, integrity, and flow assurance).

- Capital flow: Strong gold prices support mining majors’ budgets → potential partnerships or repurposing of O&G subsea infrastructure for mineral transport.

- Transition angle: Gold’s role as a hedge accelerates energy transition funding (renewables, hydrogen) — more offshore wind + geothermal + CCUS projects.

Key Takeaways for Subsea & Pipeline Professionals

- Oil & gas: Focus on cost-efficient brownfields, HPHT tiebacks, and life extension.

- Gold rally: Watch for mining capex spillover into slurry pipelines and subsea tech.

- Energy transition: Offshore wind, geothermal, and hydrogen pipelines gain momentum your expertise is more relevant than ever.

What do you think? Is the gold rally creating new pipeline opportunities in your network, or is oil & gas discipline the bigger story for 2026?

Comment below : share this post!

Stay tuned for more HPHT, subsea integrity, and energy transition insights.

Gig ’em!#OilAndGas2026 #GoldMarket #EnergyTransition #SubseaPipelines #HPHT #GigEm #AggieEngineers