Oko Immanuel

Petroleum / Subsea Engineer

Founder, Offshore Pipeline Insight

Texas A&M Alumnus.

March 06, 2026

Floating offshore wind represents a transformative advancement in renewable energy deployment, enabling access to high-wind-resource sites in water depths typically exceeding 60 meters where fixed-bottom foundations become technically or economically unfeasible. As a subsea and pipeline engineer, I see significant synergies between floating wind and established offshore oil & gas infrastructure particularly in dynamic export cabling, mooring systems, and subsea tie-ins for hybrid energy hubs or green hydrogen production.This technical blog provides a detailed examination of floating offshore wind technology, market status as of early 2026, key engineering comparisons, cost trends, and emerging project highlights.

1. Fundamental Engineering Concepts and Foundation Types

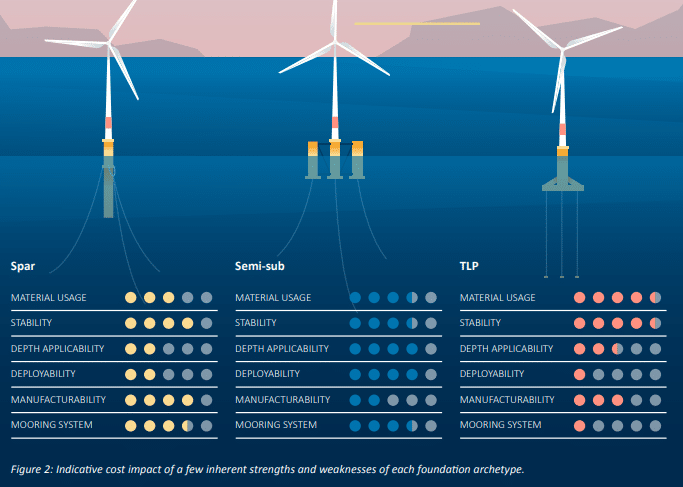

Floating platforms must provide sufficient buoyancy, stability against wave/wind loading, and station-keeping via mooring systems, while minimizing motion to maintain turbine performance.The three primary floating foundation archetypes are:

- Spar: Deep-draft cylindrical buoy with high ballast for low center of gravity; excellent stability but high material usage and challenging tow-out/installation.

- Semi-submersible (Semi-sub): Multi-column pontoon design with spread mooring; balances stability, manufacturability, and depth applicability; widely adopted for scalability.

- Tension Leg Platform (TLP): Vertically tensioned tendons minimize heave/pitch/roll; superior motion performance but higher mooring complexity and cost.

Here is a comparative diagram illustrating the inherent strengths and cost impacts of these archetypes:

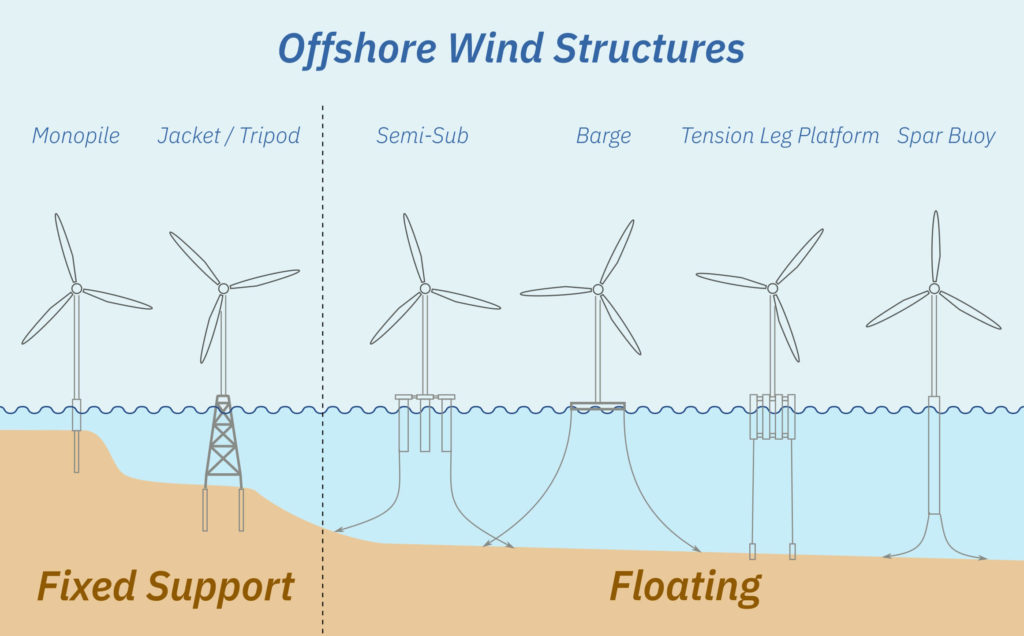

This overview diagram shows the full spectrum of offshore wind structures, clearly distinguishing fixed (monopile, jacket/tripod) from floating types:

2. Floating vs. Fixed-Bottom:

Technical Comparison

Fixed-bottom systems dominate shallow waters (<60 m) due to proven reliability and lower LCOE. Floating systems excel in deeper waters by decoupling from seabed conditions.Key differentiators:

- Fixed: Direct seabed interface; high fatigue resistance but limited to continental shelves.

- Floating: Dynamic response to environmental loads; requires advanced hydrodynamic modeling, active ballast control, and robust dynamic power cables.

Schematic comparison of fixed monopile in shallow water versus floating semi-submersible in deep water:

(Note: The same foundational diagram above highlights this boundary effectively.)

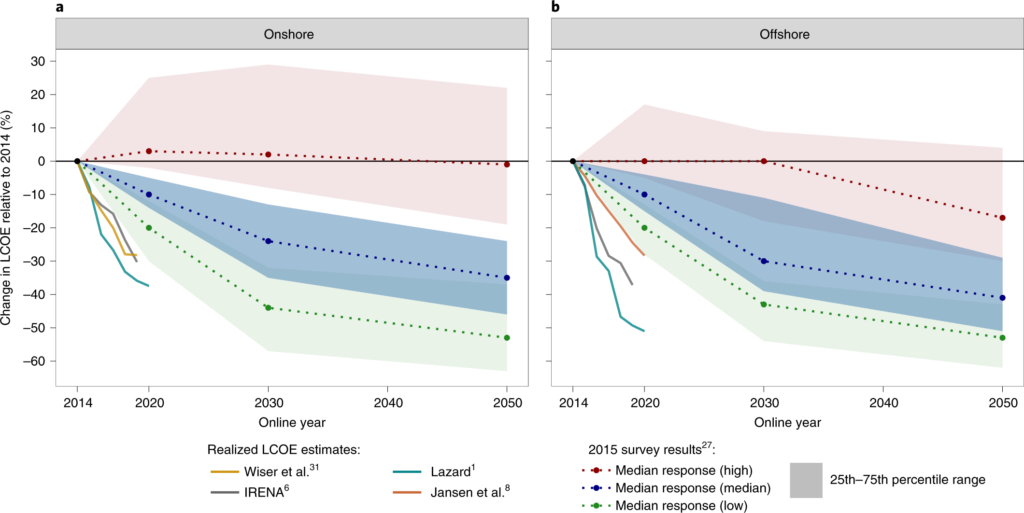

3. Levelized Cost of Energy (LCOE) Trends

LCOE for floating wind remains higher than fixed-bottom or onshore due to platform complexity, but expert projections indicate rapid convergence through scale, turbine uprating (15–20+ MW units), and supply-chain maturation.

Historical and forecasted LCOE reductions (relative to a 2014 baseline) show offshore wind achieving 30–50% declines by 2050, with floating expected to follow similar learning curves as commercial deployment accelerates.

Here is a representative graph from expert elicitation surveys illustrating projected LCOE trajectories for offshore wind:

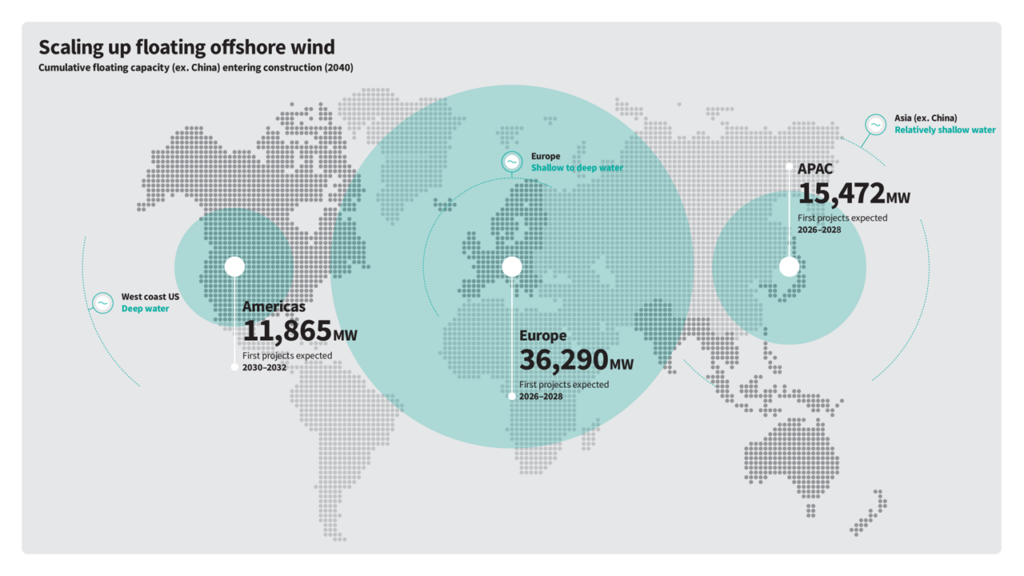

4. Global Deployment Hotspots and Project Pipeline (2026 Perspective)

As of March 2026, operational floating capacity remains limited (~270–300 MW), dominated by demonstration projects. However, the pipeline is robust, with first commercial-scale arrays targeting FID in 2026–2028 and significant capacity entering construction by 2030–2040.

Key regions include:

- Europe (Northwest and Southern): Deepwater focus, leading in GW-scale ambitions.

- Asia-Pacific (ex-China): Shallow-to-moderate depths, rapid early deployment.

- Americas (US West Coast, Brazil, Chile): Deepwater Pacific sites.

- Emerging: Africa, Eastern Europe, Oceania.

This world map highlights potential floating wind markets and geographic distribution:

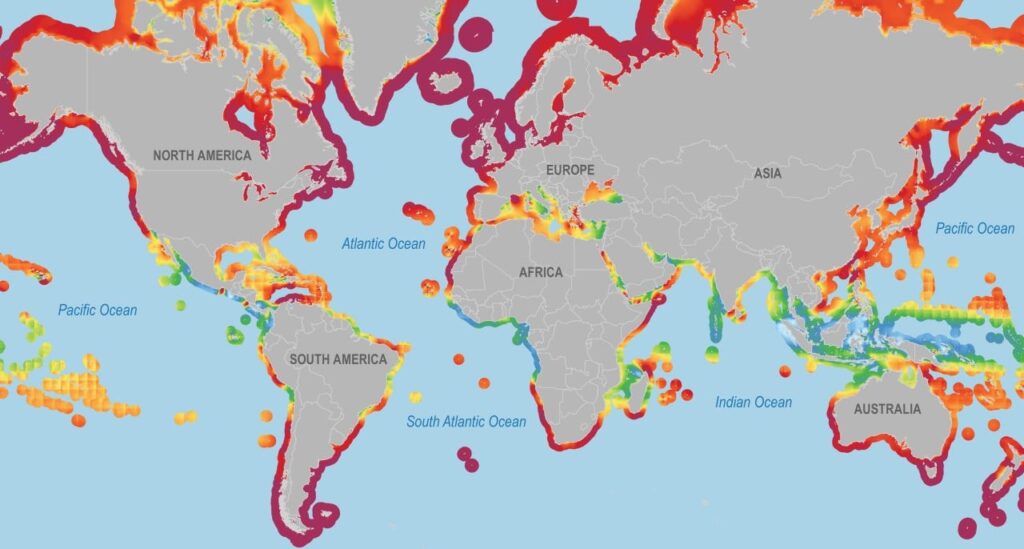

Another global resource assessment map showing high-wind areas suitable for floating deployment:

Cumulative capacity projections entering construction by 2040 (excluding China) underscore regional scaling:

Notable 2026 milestones include Japan’s Goto project (first commercial hybrid SPAR farm), UK’s Green Volt (pioneering 400–560 MW array), and port developments on the US West Coast.

Closing Thoughts: Relevance to Subsea and Pipeline Engineering

Floating wind demands expertise in dynamic umbilicals, power export cables, mooring integrity, and subsea infrastructure areas where oil & gas experience transfers directly. Opportunities exist in repurposing existing pipelines for CO₂ transport from offshore hubs or integrating floating wind with gas-to-power systems.

The sector is transitioning from pilot to commercial viability, with engineering challenges being addressed through standardization and digital twins. As costs decline and deployments scale, floating offshore wind will play a pivotal role in the energy transition.

What specific aspect mooring analysis, dynamic cable fatigue, or hybrid concepts would you like explored in more depth?

Oko Immanuel

Petroleum / Subsea Engineer

Founder, Offshore Pipeline Insight

Texas A&M Alumnus.

March 06, 2026