By Oko

Founder, Offshore Pipeline Insight

March 13, 2026

Floating offshore wind (FOW) technology is undergoing a transformative “commercialization leap” in 2026, shifting from small-scale pilots and demonstrations to multi-gigawatt (GW) deployments. This leap is driven by maturing supply chains, policy support, technological standardization, and plummeting costs, unlocking vast deep-water resources where fixed-bottom turbines are infeasible. With global installed FOW capacity reaching 278 MW by the end of 2024, the sector has now secured routes to market for over 2.4 GW, signaling industrial-scale viability. Projections indicate 4.1 GW installed or underway by 2030, surging to 56.2 GW by 2040, as nations like the UK (targeting 5 GW by 2030) and the US (15 GW by 2035) ramp up ambitions. This blog dives into the technical enablers, key projects, economic drivers, and future outlook propelling FOW toward mainstream energy production.

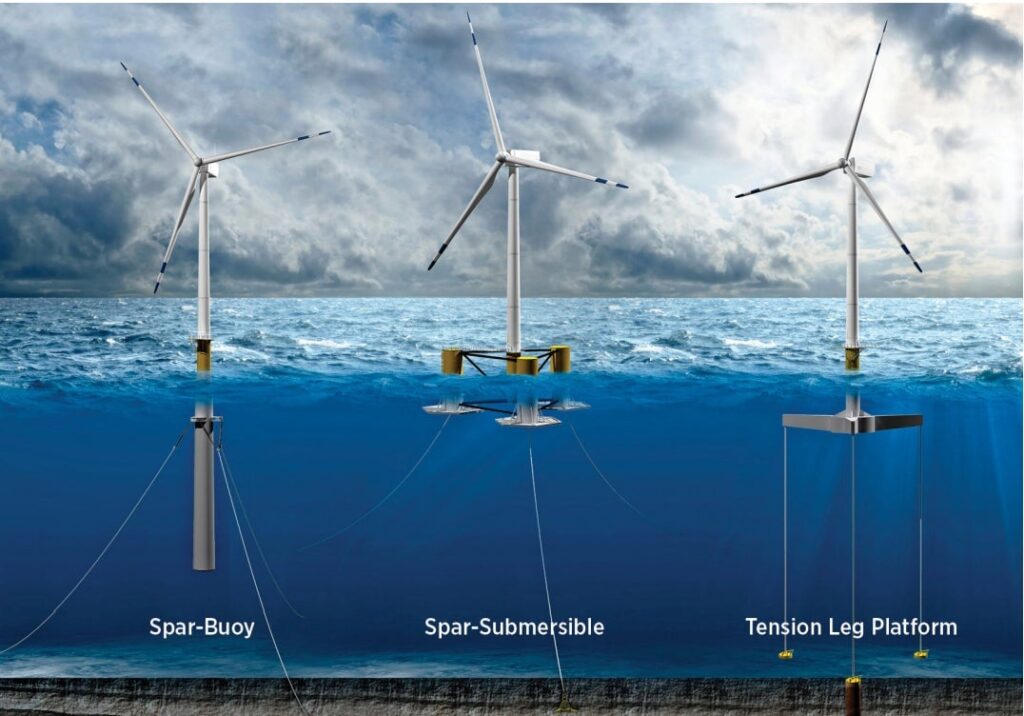

Technological Foundations: Platform Designs and InnovationsAt the heart of FOW’s commercialization is the evolution of floating platforms, adapted from oil and gas mooring expertise. Three primary types dominate: spar-buoy (deep draft for stability via ballast), semi-submersible (wide base for buoyancy and wave resistance), and tension leg platform (TLP, with taut vertical moorings for minimal motion). These designs enable deployment in water depths exceeding 60 meters, accessing stronger, more consistent winds.Standardization is key to the leap platforms are now modular, with lighter materials (e.g., high-strength steel and composites) reducing topside weight by up to 70% in advanced concepts. Larger turbines (15–20 MW class) integrate seamlessly, boosting capacity factors to 50–60%. Dynamic cable systems and advanced mooring (synthetic ropes over chains) enhance durability against harsh marine conditions.

This diagram illustrates the main FOW platform types, showing how each anchors to the seabed while supporting massive turbines.Innovations like active ballast control and digital twins for predictive maintenance are de-risking operations, paving the way for serial production.

Key Milestones and Projects Driving Commercialization

2026 marks a pivotal year, with early 2026 awards adding 193 MW to the global pipeline via the UK’s Allocation Round 7 (AR7). Landmark projects exemplify the leap:

- Hywind Scotland (Equinor) The world’s first commercial FOW farm (30 MW, operational since 2017) uses spar-buoy platforms. Its success has spawned Hywind Tampen (88 MW, Norway), powering oil platforms and demonstrating hybrid energy applications.

Aerial view of Hywind Scotland’s spar-buoy turbines floating off the Scottish coast, a pioneer in commercial FOW.

- Green Volt (UK): A 560 MW project by Flotation Energy and Vårgrønn, securing a CfD at £139.93/MWh in 2024. Targeting FID in mid-2026 and commissioning by 2029, it integrates with oil and gas infrastructure for dual-use electrification.

- Bandibuli (South Korea): 750 MW awarded in 2025, highlighting Asia’s growth.

- French tenders (AO5/AO6): 750 MW at competitive prices (€85.5–92.7/MWh), accelerating Europe’s pipeline.

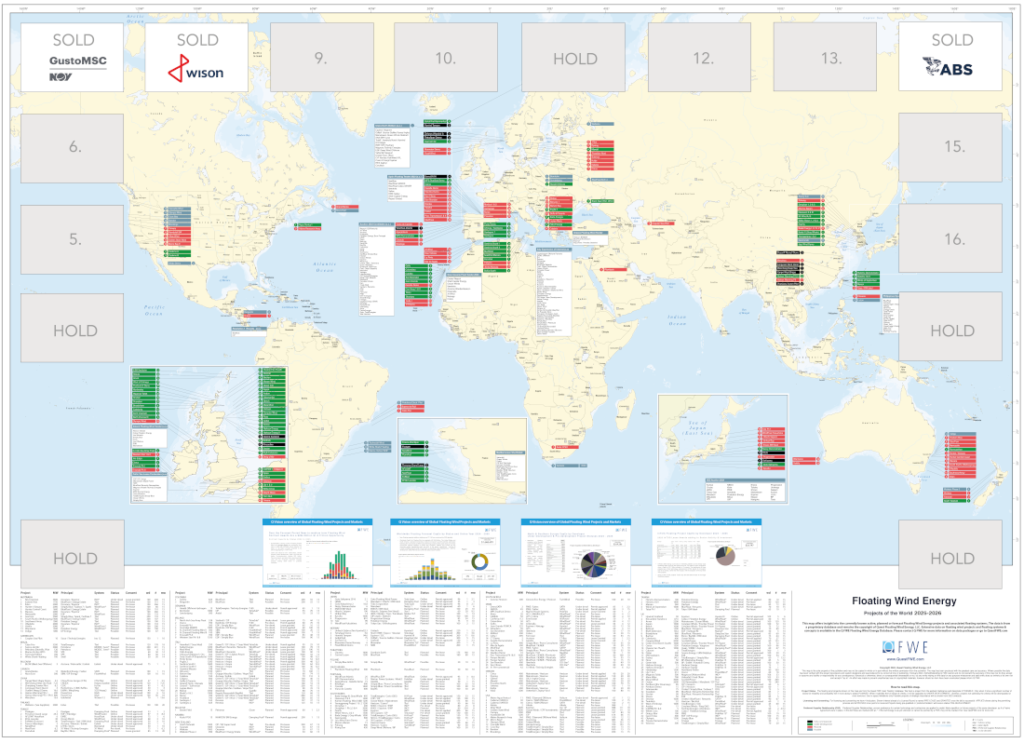

Globally, over 150 GW is in planning, with multi-GW hubs in the UK, France, South Korea, and emerging US West Coast leases.

This global map outlines FOW projects as of 2026, showing concentrations in Europe, Asia, and North America.

Cost Reductions and Economic Viability

The commercialization leap hinges on dramatic cost drops. Levelized cost of energy (LCOE) for FOW has fallen from over $200/MWh in early pilots to $100–150/MWh today, projected to reach $50–75/MWh by 2030 through scale and learning effects. Market value is booming from $2.8 billion in 2025 to $5.38 billion in 2026, with a 92.1% CAGR. Drivers include turbine upsizing (reducing per-MW costs), optimized supply chains (e.g., quayside assembly), and policy incentives like CfDs and tax credits. Oil majors like OMV are leveraging FOW for asset decarbonization, integrating with subsea infrastructure.

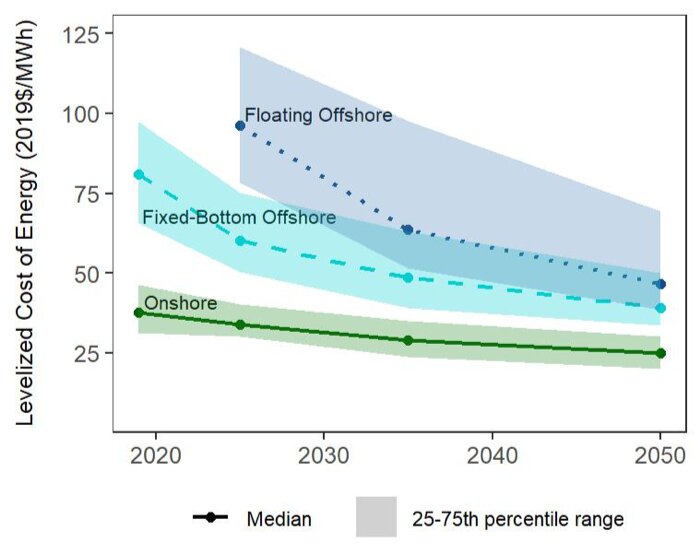

This graph depicts LCOE trajectories for onshore, fixed-bottom offshore, and floating offshore wind through 2050, highlighting FOW’s convergence with competitors.Challenges and Future InnovationsDespite progress, hurdles remain: High upfront CAPEX ($4–6 million/MW), supply chain bottlenecks (e.g., vessel shortages), and grid integration in remote deep waters. Environmental impacts, like mooring effects on marine life, require ongoing mitigation.Looking ahead, innovations such as multi-turbine arrays and hybrid wind-wave platforms promise further efficiencies. By 2030, FOW could surpass 1 GW annual installations, comprising 6.1% of global wind projects. Concepts like massive 40-MW floating arrays exemplify scalable designs.

Conceptual rendering of a large-scale FOW array, illustrating future gigawatt farms in deep seas.Tying It Together: A Sustainable Offshore FutureThe commercialization leap in floating offshore wind is reshaping the energy landscape, enabling access to 80% of untapped offshore resources and supporting net-zero goals. For offshore pipeline and energy professionals, this means opportunities in subsea moorings, dynamic cables, and hybrid infrastructure but also challenges in integrity management amid shifting vessel patterns.What are your thoughts on FOW’s role in decarbonizing offshore operations? Share in the comments—let’s advance the discussion!