By Oko

Founder, Offshore Pipeline Insight

March 13, 2026

As the global energy sector pivots toward sustainability amid maturing oil and gas fields, offshore decommissioning services have emerged as a critical, high-growth market. Decommissioning involves the safe removal or repurposing of offshore infrastructure platforms, wells, pipelines, and subsea equipment—at the end of their productive life. Driven by stringent environmental regulations, aging assets in regions like the North Sea and Gulf of Mexico (GoM), and the push for net-zero transitions, this sector is not just about dismantling; it’s about responsible closure, recycling, and even asset repurposing for renewables like carbon capture and storage (CCS) or offshore wind. In 2026, with over 600 platforms slated for removal in Europe alone and global spending ramping up, understanding market dynamics and technical nuances is essential for industry stakeholders. This blog explores the latest market size, share breakdowns, technical processes, and future trends.

Market Size and Growth ProjectionsThe global offshore decommissioning services market is experiencing robust expansion, fueled by regulatory mandates (e.g., OSPAR Convention in Europe, BSEE rules in the US) and the maturation of legacy fields installed in the 1970s-1990s. According to recent analyses, the market was valued at approximately USD 7.53-8.08 billion in 2025, growing to USD 8.08-9.07 billion in 2026. Projections indicate a compound annual growth rate (CAGR) of 7-8% through 2030-2034, potentially reaching USD 11.52-19.7 billion by 2031-2034. This growth is accelerated by increasing decommissioning obligations—over 10,000 wells and 2,000 platforms worldwide are due for action in the next decade—amid falling oil prices and energy transition pressures.

Key drivers include:

- Regulatory Push: Stricter environmental compliance, with “Rig-to-Reef” programs allowing partial structure retention for marine habitats, reducing costs by 20-30%.

- Asset Maturity: North Sea alone anticipates USD 50-60 billion in spending through 2040.

- Sustainability Focus: Integration with CCS and hydrogen projects, repurposing pipelines and platforms.

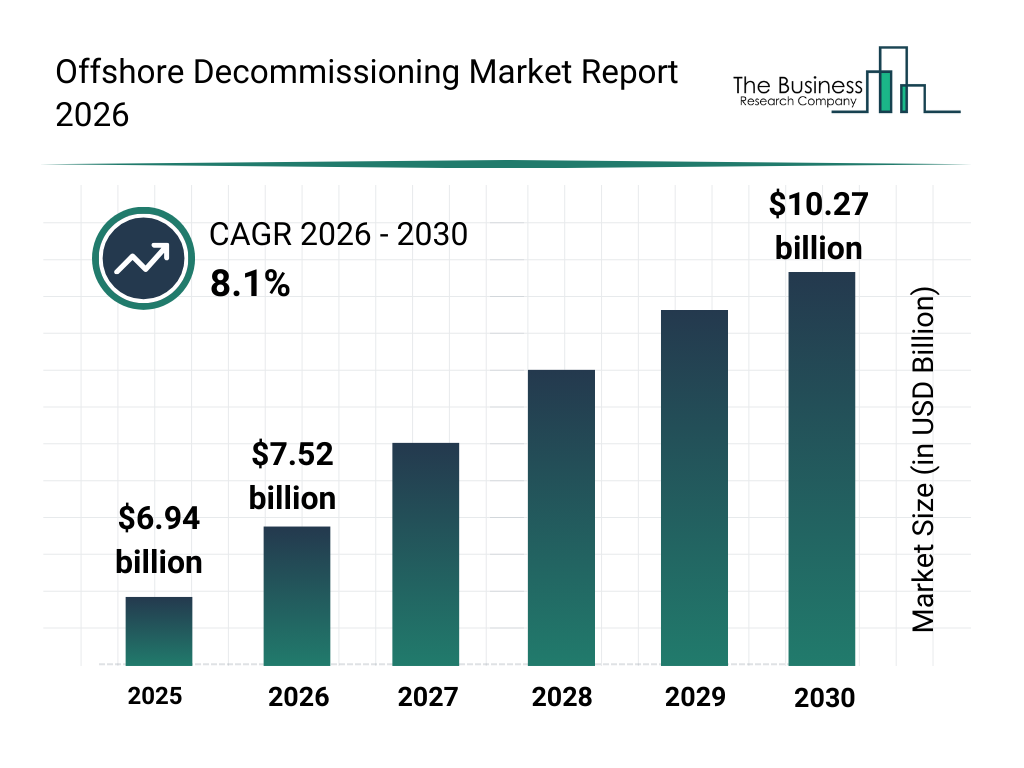

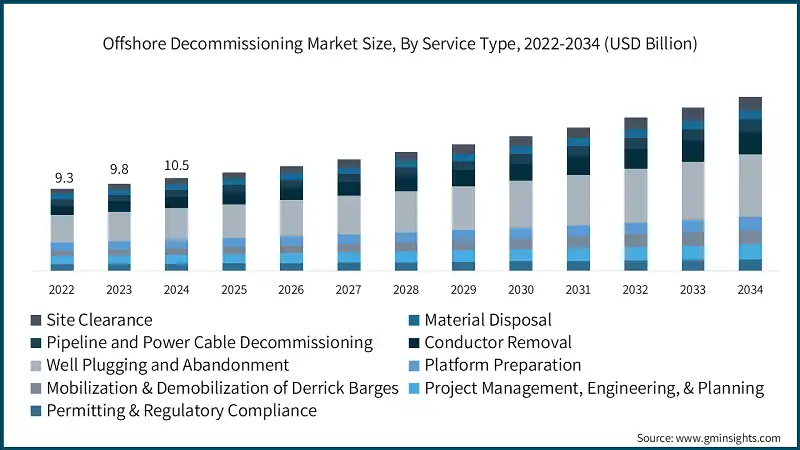

This bar chart illustrates the projected market size growth from 2025 to 2030, highlighting a steady upward trajectory at an 8.1% CAGR. Another view of market segmentation by service type over time:

Market Share BreakdownThe market is fragmented, with major players like Aker Solutions, Oceaneering International, Wood Group, and Saipem holding significant shares through integrated services. By service type:

- Well Plugging and Abandonment (P&A): Dominates with ~31-35% share in 2025, involving cementing and sealing wells to prevent leaks—critical for environmental safety and projected to grow at 7-8% CAGR.

- Platform Removal: Topsides and substructure removal segments are fastest-growing (8-9% CAGR), driven by heavy-lift vessel innovations.

- Pipeline and Cable Decommissioning: Accounts for 15-20%, focusing on subsea infrastructure integrity.

- Others (e.g., site clearance, materials disposal): 20-25%, emphasizing recycling rates up to 95% for steel.

By water depth:

- Shallow Water (<200m): 60-70% share, primarily in GoM and North Sea, easier access but high volume.

- Deepwater/Ultra-Deepwater: Growing at 9%+ CAGR, with challenges in depths >1,000m requiring ROVs and advanced robotics.

Regional shares:

- Europe: Leads with 45-50% (USD 4.52 billion in 2026), thanks to North Sea maturity—UK and Norway account for 70% of regional activity.

- North America: 25-30%, dominated by US GoM with 2,000+ platforms pending.

- Asia-Pacific: Emerging at 15%, with Australia and Malaysia ramping up.

- Rest of World: 10-15%, including Brazil and West Africa.

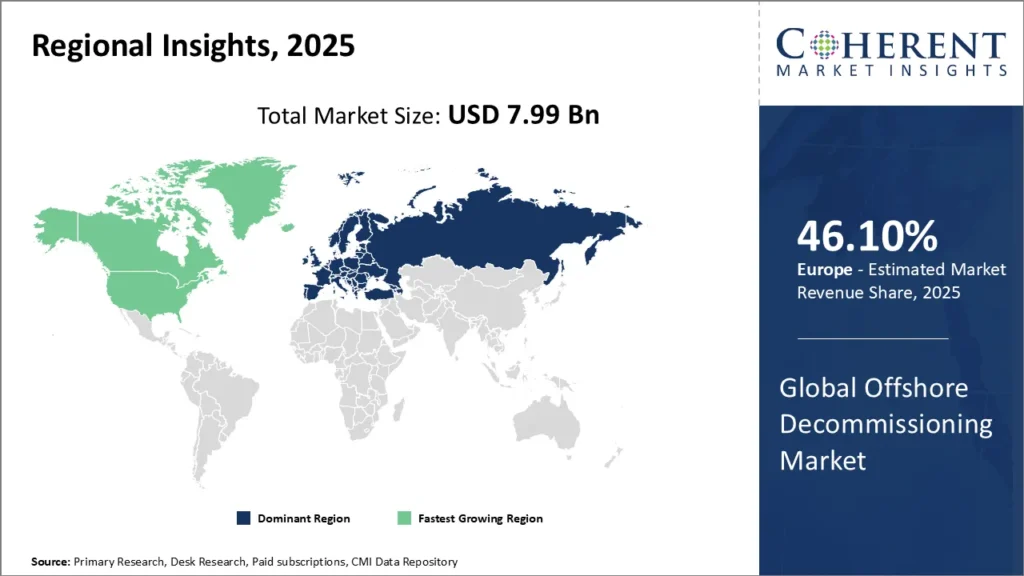

This world map shows regional revenue shares, with Europe as the dominant player at 46.1% in 2025.

Technical Aspects of Offshore Decommissioning

Decommissioning is a multi-phase, technically intensive process governed by standards like API RP 2SIM and ISO 19901-9. Key stages include:

- Project Management and Planning: Initial surveys using ROVs/AUVs for asset condition assessment, regulatory permitting (e.g., NEPA in US), and engineering simulations for load analysis.

- Well P&A: Involves perforating, cementing, and barrier installation to isolate reservoirs. Techniques like rigless P&A reduce costs by 40%, using coiled tubing or wireline.

- Platform Preparation and Removal: Topsides (decks/modules) are cut and lifted via heavy-lift vessels (e.g., Pioneering Spirit with 48,000-ton capacity). Substructures (jackets) may be toppled, partially removed, or fully extracted using explosives or mechanical cutters.

- Pipeline and Cable Decommissioning: Flushing, pigging, and burial/removal to prevent hazards. Dynamic positioning vessels ensure precision in deepwater.

- Site Clearance and Disposal: Seabed verification via multibeam sonar, materials recycling (steel smelted, hazardous waste treated). “Rig-to-Reef” converts structures into artificial reefs, saving 10-20% on costs.

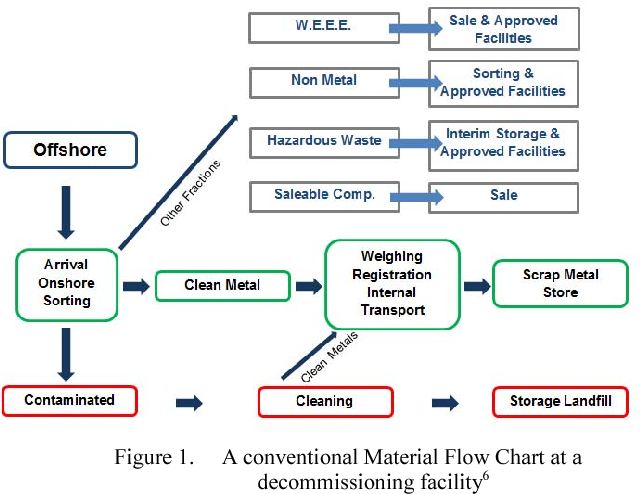

This flow chart depicts a conventional material handling process at a decommissioning facility, from offshore arrival to final disposal or recycling.Innovations include AI-driven predictive modeling for fatigue analysis, hybrid vessels for lower emissions, and modular cutting tools for subsea efficiency.

Challenges and Opportunities

Challenges:

- High Costs: Average platform decommissioning at USD 20-100 million, with deepwater escalating to USD 500 million+ due to weather delays and supply chain issues.

- Environmental Risks: Potential leaks or habitat disruption; mitigated by real-time monitoring.

- Regulatory Variations: Fragmented global rules slow projects.

Opportunities:

- Repurposing: Converting assets for CCS (e.g., Northern Lights project) or hydrogen storage, extending value.

- Supply Chain Growth: Demand for specialized vessels and robotics boosts market entry.

- Sustainability Gains: High recycling rates align with ESG goals, attracting investment.

By 2030, the market could see 20% integration with renewables, reducing net costs through hybrid projects.

Looking Ahead: Implications for the Offshore Sector

The offshore decommissioning services market’s expansion to USD 10+ billion by 2030 underscores its role in the energy transition, balancing legacy cleanup with future-proofing. For pipeline integrity pros, this means heightened focus on subsea assessments, repurposing opportunities, and collaboration with decommissioning specialists.What are your experiences with decommissioning projects?

Share in the comments—let’s discuss strategies for cost-effective, sustainable outcomes!