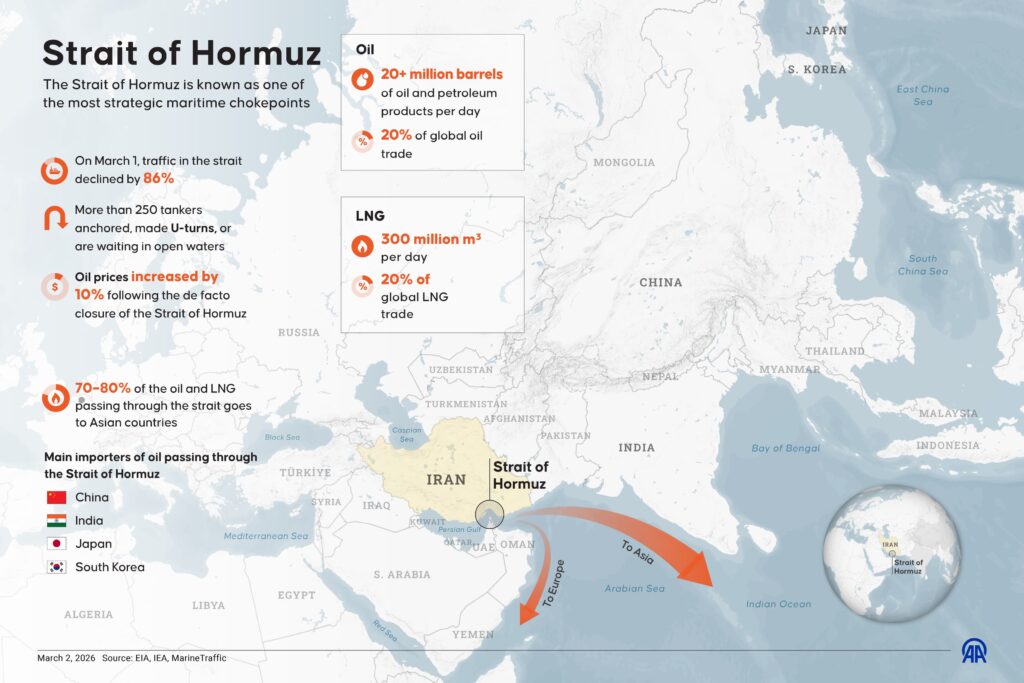

The Strait of Hormuz, a narrow waterway connecting the Persian Gulf to the Arabian Sea, stands as one of the world’s most critical maritime chokepoints. Often described as the “jugular vein” of global energy supplies, it facilitates the passage of approximately 20-21 million barrels of oil per day equivalent to about 20% of global oil trade and a similar share of liquefied natural gas (LNG). In the context of March 11, 2026, amid the ongoing US-Israel-Iran conflict (dubbed “Operation Epic Fury”), the Strait has become a flashpoint, with tanker traffic plummeting 70-90% due to missile strikes, insurance pullbacks, and warnings from Iranian forces. This deep dive explores its geography, strategic importance, historical conflicts, and current economic ramifications.

Geography and Strategic Role

The Strait of Hormuz is a 33-kilometer-wide channel at its narrowest point, flanked by Iran to the north and Oman to the south. It serves as the sole maritime exit for oil and gas exports from major producers like Saudi Arabia, Iraq, Kuwait, Qatar, the UAE, and Iran itself accounting for over 40% of the world’s oil and 20% of gas production. The waterway’s shallow depths (averaging 50-100 meters) and congested shipping lanes make it vulnerable to disruption; a single tanker sinking could block traffic for days.

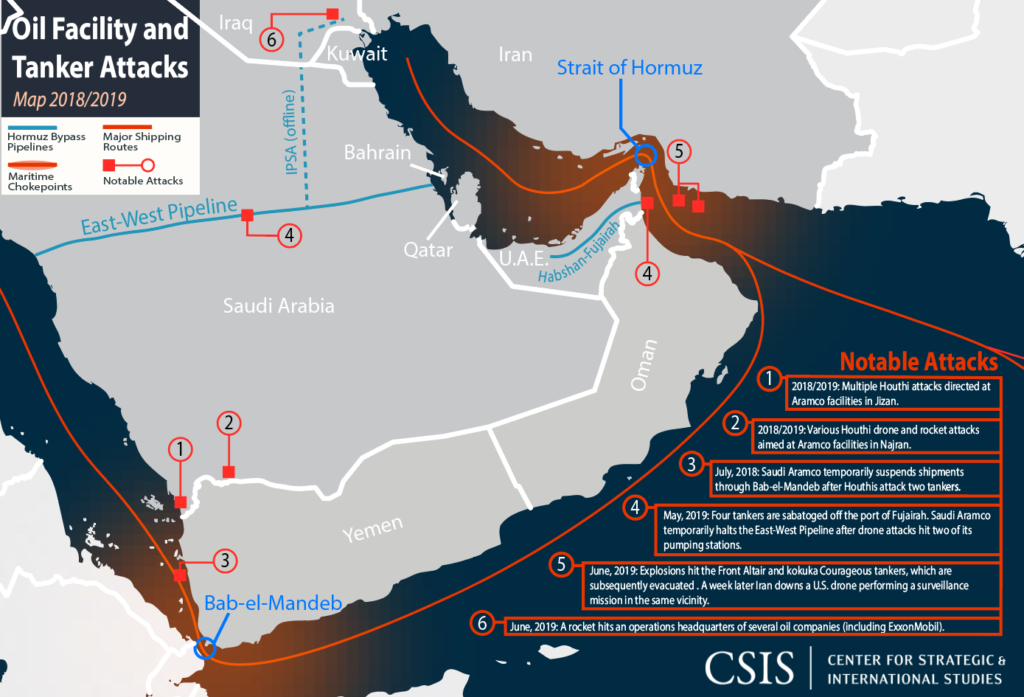

Figure 1: Map of the Strait of Hormuz, highlighting oil tanker routes, attack sites from recent conflicts, and key choke points. This illustrates the Strait’s exposure to threats, with major routes bypassing potential blockades like the East-West Pipeline in Saudi Arabia. Key importers reliant on Hormuz flows include China (70-80% of its Middle East oil), India, Japan, and South Korea, making any closure a global supply shock. Europe, too, faces risks, with gas prices surging 60% amid depleted inventories. Historical and Geopolitical ConflictsThe Strait has been a hotspot for decades, from the Iran-Iraq War (1980s “Tanker War,” where mines disrupted flows) to US-Iran tensions in the 2010s. Iran’s asymmetric warfare doctrine—using speedboats, missiles, and drones—has long targeted the waterway as leverage against sanctions or attacks. In 2026, the conflict escalated with US-Israel strikes on Iranian nuclear sites (February 28 onward), leading Iran to radio warnings against transit and missile strikes on tankers. Traffic has dropped to 10-15% of pre-conflict levels, not from physical blockades but commercial fears (insurers canceling war risk cover, operators halting voyages). President Trump’s administration views closure as a “red line,” but Iran retains capacity to prolong disruptions despite military degradation. The US could release strategic reserves, but prolonged conflict risks $100+ oil barrels, inflation spikes, and economic drag (0.2-0.4 ppt on US PCE inflation per 10% gasoline rise).

Figure 2: Infographic of Hormuz flows, showing 20+ million barrels of oil daily, 20% of global LNG, and major importers like China and India. Traffic has declined 86% since March 1, with over 250 tankers anchored or rerouting

Economic and Energy Ramifications

A sustained closure could shatter global markets: Oil prices have already climbed amid fears, with Europe facing winter shortages and Asia (China’s 13% of imports via Hormuz) hit hardest. Logistics disruptions add pressure, potentially stalling growth and forcing ECB/Fed rate rethink. Alternatives like Saudi’s East-West Pipeline exist but can’t fully compensate. In summary, Hormuz’s closure—whether physical or commercial—threatens energy security, amplifying calls for diversified routes and renewables.

Deep Dive: Carbon Capture Pipelines – Technology, Design, Integrity, and Safety in CCS

Carbon capture and storage (CCS) pipelines are pivotal in the energy transition, transporting captured CO₂ from industrial sources to storage sites for sequestration or utilization. As of 2026, CCS is scaling rapidly, with global operational capacity growing and a pipeline of projects aiming for 50,000–150,000 km of new infrastructure by 2050 in the US alone. This deep dive covers the technology, design principles, integrity management, safety protocols, and 2026 advancements.

Technology and Process Overview

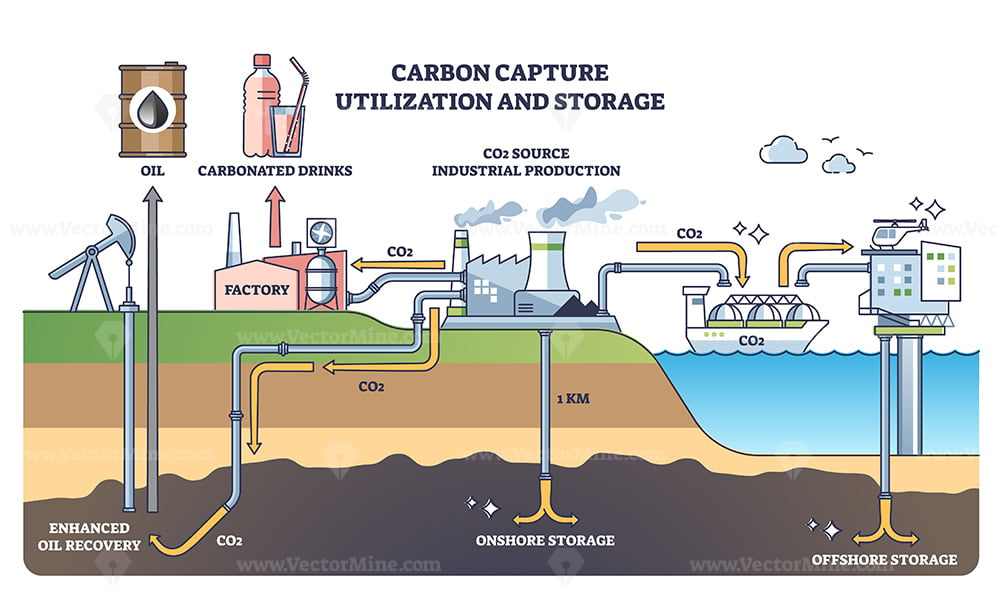

CCS pipelines transport CO₂ in dense (supercritical) phase for efficiency, typically at pressures above 7.38 MPa and temperatures 31–50°C. The system includes:

- Capture: From industrial sources (power plants, cement/steel factories) using solvents, membranes, or sorbents like metal-organic frameworks (MOFs).

- Compression/Conditioning: To supercritical state, removing impurities (water, H₂S) to prevent corrosion.

- Transport: Via dedicated pipelines (often repurposed from oil/gas).

- Storage/Utilization: Injection into saline aquifers, depleted reservoirs, or use in enhanced oil recovery (EOR), carbonated drinks, or chemicals.

Figure 3: Diagram of a CCS pipeline system, showing CO₂ capture from industrial sources, transport, onshore/offshore storage, and enhanced oil recovery. Impurities and high pressures demand specialized design.

Design and Construction

Pipelines use high-strength steel (API 5L X60/X70) with corrosion-resistant coatings and cathodic protection. Key considerations:

- Fracture Control: CO₂ decompression can cause running fractures—designs include crack arrestors and thicker walls.

- Impurities Management: Limits on water (<50 ppm) and H₂S to avoid embrittlement.

- Routing: Avoid populated areas; offshore lines use subsea tech like J-lay.

- 2026 Innovations: DNV’s Skylark JIP advances safety modeling for dense CO₂.

Integrity and Safety

Integrity focuses on preventing leaks via PHMSA rules (49 CFR 195 for liquids, updated for CO₂). Techniques:

- In-Line Inspection (ILI): MFL/UT for corrosion/cracks.

- Direct Assessment: ECDA/ICDA for external/internal threats.

- Monitoring: Real-time sensors for pressure, temperature, leaks.

- Safety Protocols: Emergency shutdown valves, rupture mitigation, public awareness programs.

- Risks: Supercritical CO₂’s asphyxiation hazard and dispersion modeling for plumes.

PHMSA’s coalition letter (March 2026) calls for modernized CO₂ rules, emphasizing integrity in CCS build-out. The US DOE’s supply chain review notes low risk for CCS scaling, with 390k–1.8M jobs potential.

2026 Outlook and Challenges

Global CCS capacity is expanding, with tech compendiums highlighting capture innovations (e.g., MOFs, surface-modified sorbents). Challenges include cost (transport ~$5–20/tonne/km), public acceptance, and repurposing existing pipelines (e.g., for H₂/CO₂ blends). Conferences like Carbon Capture USA 2026 emphasize infrastructure build-out for net-zero.In essence, CCS pipelines are essential for decarbonizing hard-to-abate sectors, with design and integrity evolving to ensure safe, scalable deployment.