By Oko Immanuel, M.Eng – Founder, Offshore Pipeline Insight

March 19, 2026

The offshore energy sector in 2026 is facing one of its most acute logistical bottlenecks in decades: intensifying competition for marine vessels and specialized labor between traditional oil & gas (especially deepwater HPHT developments) and the rapidly scaling offshore wind industry (particularly floating wind in frontier waters).Late 2026 forecasts from analysts (Rystad Energy, Westwood Global Energy, Wood Mackenzie) point to capacity constraints building sharply as a new wave of deepwater oil & gas projects reaches final investment decision (FID), while floating wind installation campaigns accelerate in the North Sea, U.S. West Coast, Atlantic Margin, and emerging basins.

The result is a real fight for resources vessels, crews, ports, and equipment that is already driving up day rates, delaying schedules, and forcing operators to rethink project timelines and contracting strategies.

1. The Two Sides of the Competition

- Oil & Gas (Deepwater HPHT)

- New FIDs in 2026 (e.g., BP Kaskida, Beacon Shenandoah South expansions, Chevron Anchor follow-ons, Guyana Stabroek phases, Brazil pre-salt tiebacks).

- Require ultra-deepwater drillships, heavy-lift construction vessels (10,000+ tonne cranes), DP3 installation vessels, ROV/AUV spreads, and pipe-lay vessels.

- High-spec HPHT work demands experienced crews (saturation divers, subsea engineers, dynamic positioning operators).

- Offshore Wind (Floating & Fixed)

- Massive installation campaigns: U.S. West Coast (California OCS >1,000 m depths), UK North Sea extensions, Norway, Scotland, Japan.

- Need the same scarce vessels: heavy-lift crane barges for turbine foundation deployment, cable-lay vessels (dynamic export cables), SOVs (service operation vessels), CTVs (crew transfer vessels), and anchor-handling tug supply (AHTS) vessels for mooring installation.

- Require specialized labor: turbine technicians, cable jointers, geotechnical engineers, and offshore wind-specific safety training.

Both sectors compete for the same limited global fleet of high-spec vessels and the same pool of skilled personnel especially in shared basins (North Sea, U.S. GoM, Atlantic Margin).

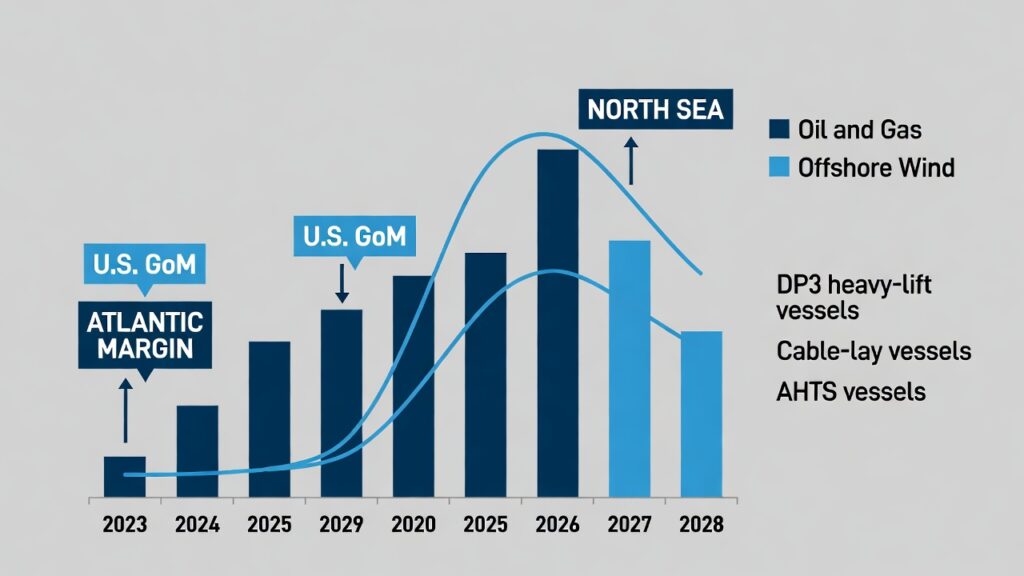

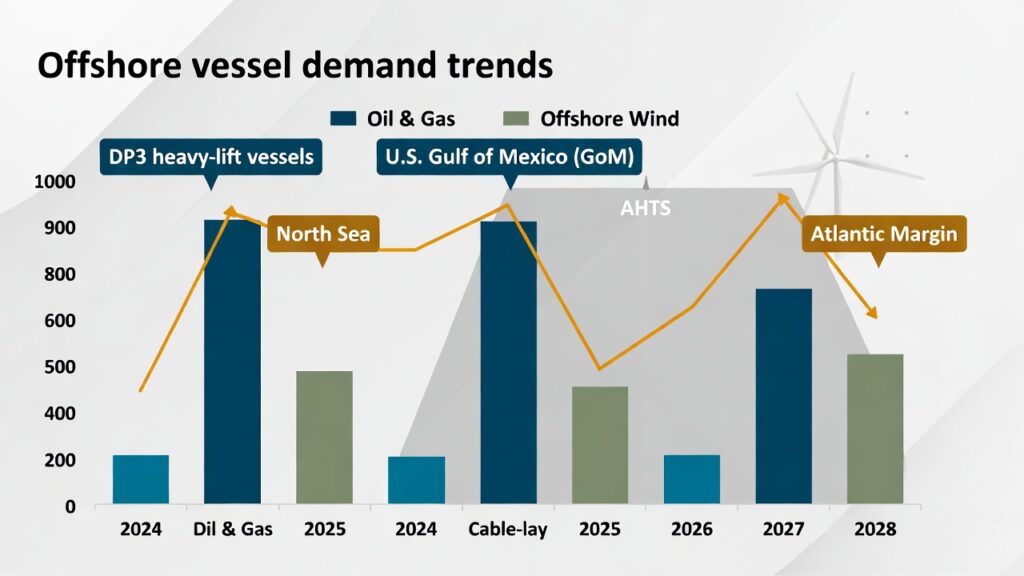

Figure 1: Vessel Demand Overlap – HPHT Oil & Gas vs. Offshore Wind (2026–2030)

( image: Dual bar/line chart showing rising demand for DP3 heavy-lift vessels, cable-lay vessels, and AHTS in both sectors. Highlight overlapping peaks in late 2026–2028, with callouts for North Sea, U.S. GoM, and Atlantic Margin.)

2. Capacity Constraints Building in Late 2026Forecasts indicate a tightening market:

- Heavy-lift & construction vessels: Global fleet utilization already >85% in Q1 2026 (Rystad). New FIDs in deepwater HPHT + floating wind campaigns will push utilization toward 95%+ by late 2026.

- Cable-lay vessels: Only ~15–20 high-spec vessels worldwide capable of deepwater dynamic cable installation. Both sectors need them simultaneously.

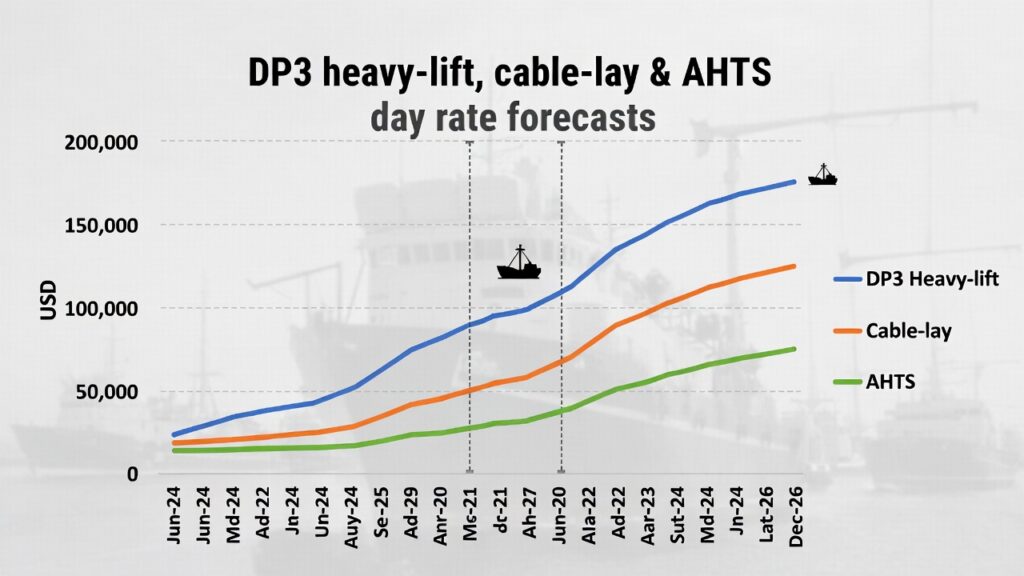

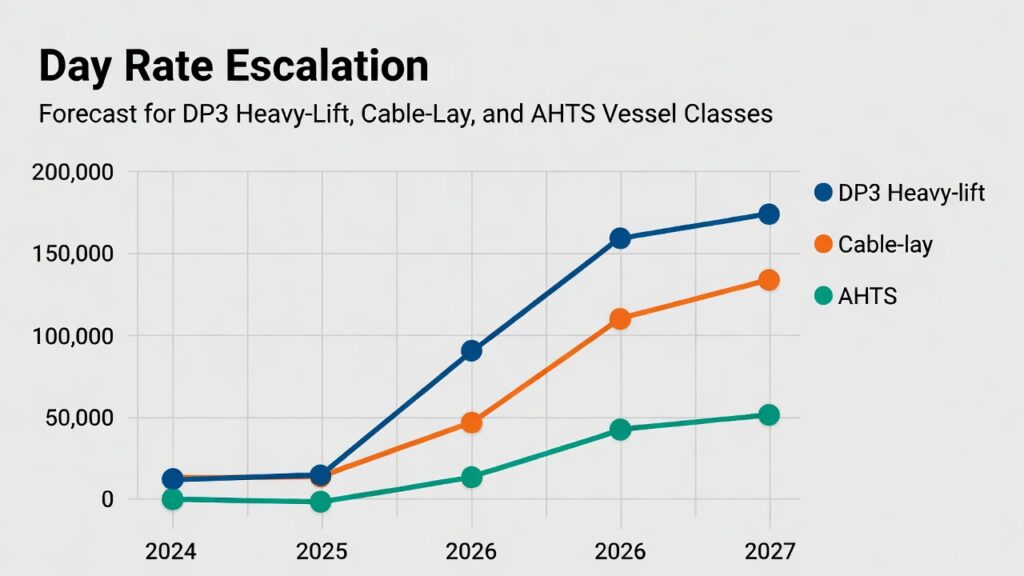

- Day rates: Already rising DP3 heavy-lift vessels quoted at $400k–$700k/day in 2026, up 30–50% from 2024 levels. Further increases expected.

- Crew shortages: Saturation divers, DP operators, and subsea engineers are in short supply. Offshore wind requires additional specialized training, pulling talent from oil & gas.

Figure 2: Offshore Vessel Day Rate Trends (2024–2026)

( image : Line chart showing day rate escalation for key vessel classes: DP3 heavy-lift, cable-lay, AHTS. Highlight upward trend starting mid-2025, with peaks forecast for late 2026.)

3. Strategies Operators Are Using to Survive the Competition

- Multi-purpose contracting: Shared vessel charters across oil & gas tiebacks and wind farm installations in the same region (e.g., Equinor in North Sea).

- Early booking & long-term deals: Locking in vessels 18–36 months ahead.

- Hybrid hubs: Co-locating floating wind with existing platforms to share export cables, moorings, and maintenance vessels.

- Workforce crossover programs: Training HPHT saturation divers and ROV pilots for wind foundation/cable work.

- Digital planning: Digital twins and metocean forecasting to optimize weather windows and reduce vessel downtime.

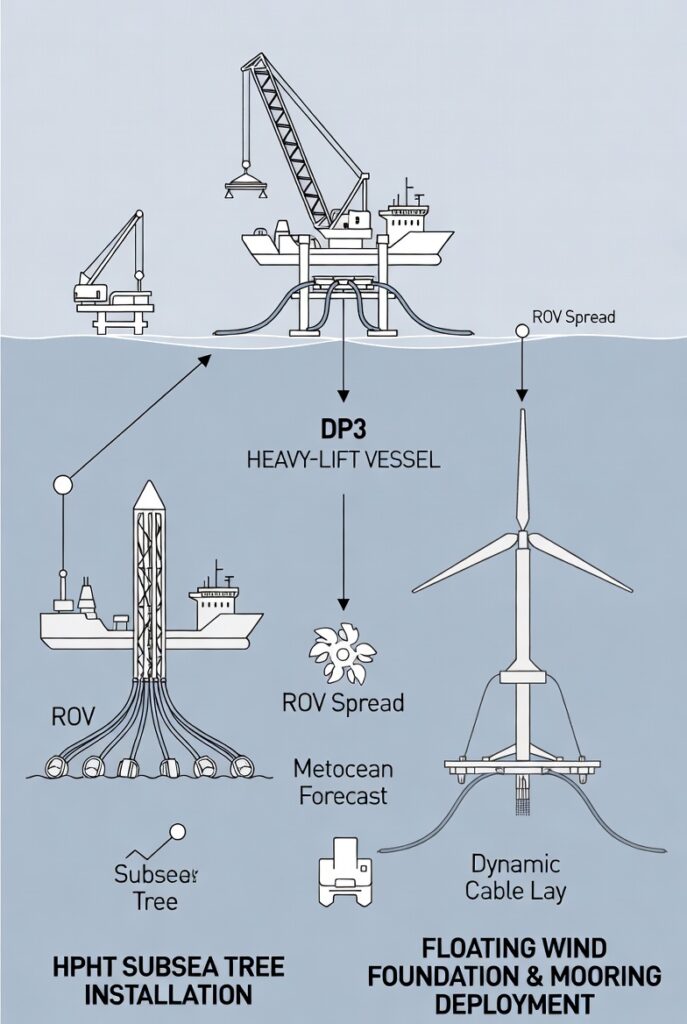

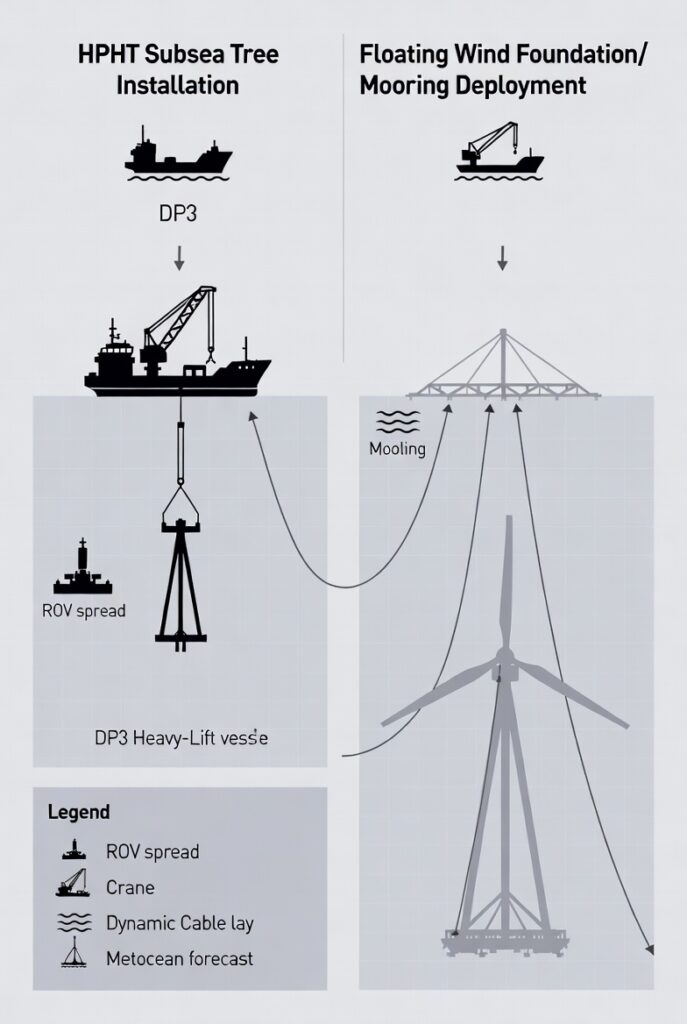

Figure 3: Hybrid Vessel Utilization Strategy

( image: Diagram showing one DP3 heavy-lift vessel performing HPHT subsea tree installation in one campaign and floating wind foundation/mooring deployment in another. Shared icons: ROV spread, crane, dynamic cable lay, metocean forecast.)

The Bottom Line for Late 2026

The fight for maritime resources is intensifying. Deepwater HPHT projects reaching FID in 2026 will collide with floating wind installation waves, creating severe capacity constraints for vessels and skilled labor.Operators who secure early contracts, embrace hybrid models, and leverage cross-industry expertise will win. Those who wait risk delays, cost overruns, and missed production windows.Engineers and offshore professionals: How are you navigating the vessel/crew competition in your region?

Share your experiences in the comments or on LinkedIn.

Stay sharp out there, brothers. The sea is crowded — but the smart ones still get through.Oko Immanuel

Subsea Engineering Specialist | Offshore Pipeline Insight