By Oko Immanuel, M.Eng – Founder, Offshore Pipeline Insight

March 19, 2026

The offshore energy sector in 2026 is defined by two powerful, seemingly opposing forces: intense decarbonization pressure and surprisingly resilient subsea project economics, especially in complex HPHT environments. Operators are no longer treating digital transformation and emission reduction as nice-to-haves they are now core survival requirements. At the same time, subsea pricing for high-end HPHT developments in the North Sea and Gulf of Mexico remains robust, even as global oil supply temporarily outpaces demand.

This dual reality is reshaping capital allocation, technology investment, and strategic priorities across the industry.

1. Decarbonization Pressure: No Longer Optional — Now Fundamental to Survival

By 2026, regulatory, investor, and market forces have converged to make decarbonization non-negotiable.

- Regulatory tightening : EU ETS expansion, U.S. methane fees, North Sea emissions intensity targets, and BSEE/BOEM requirements for electrification and CCS integration are now enforceable.

- Investor expectations : ESG funds, pension funds, and institutional investors increasingly require net-zero alignment roadmaps. Failure to demonstrate credible Scope 1 & 2 reductions risks capital flight.

- Market signals : LNG buyers demand low-carbon intensity cargoes; oil majors face shareholder pressure to shrink upstream emissions footprints while maintaining dividends.

- Digital transformation as enabler : Operators are deploying digital twins, AI-driven predictive maintenance, subsea electrification, and real-time emissions monitoring to meet targets without sacrificing production.

Key 2026 trend:

Decarbonization is no longer a cost center it’s becoming a license to operate and a competitive differentiator. Projects without credible low-carbon pathways are being deferred or canceled.

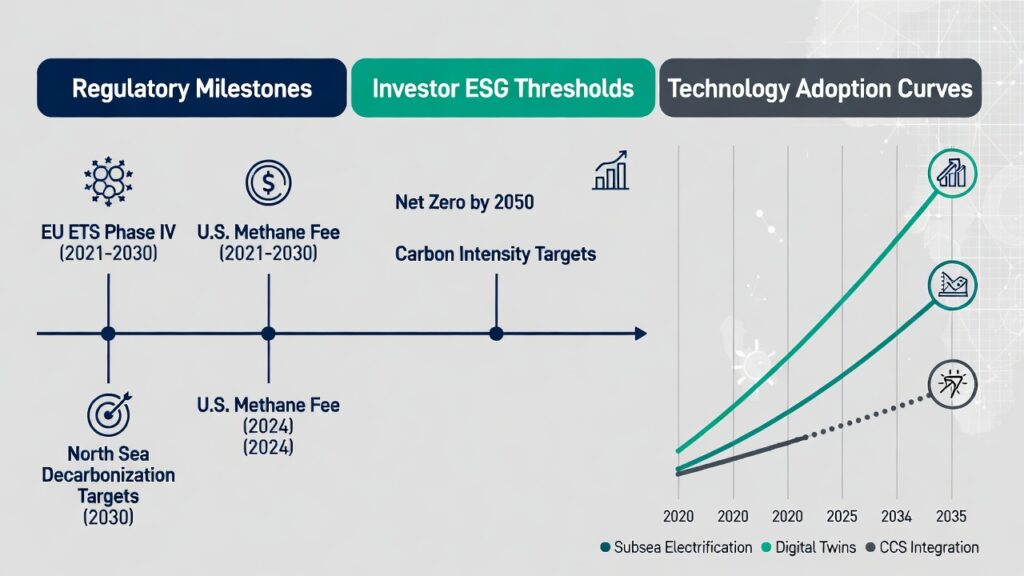

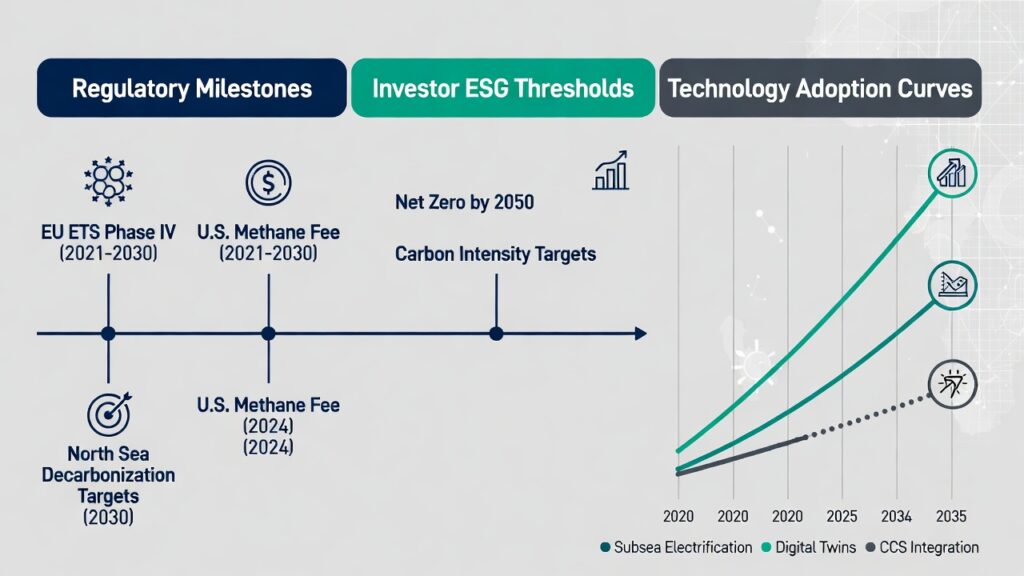

Figure 1: Offshore Decarbonization Pressure Timeline 2020–2030

(Timeline infographic showing key regulatory milestones (EU ETS, U.S. methane fees, North Sea targets), investor ESG thresholds, and technology adoption curves for subsea electrification, digital twins, and CCS integration.)

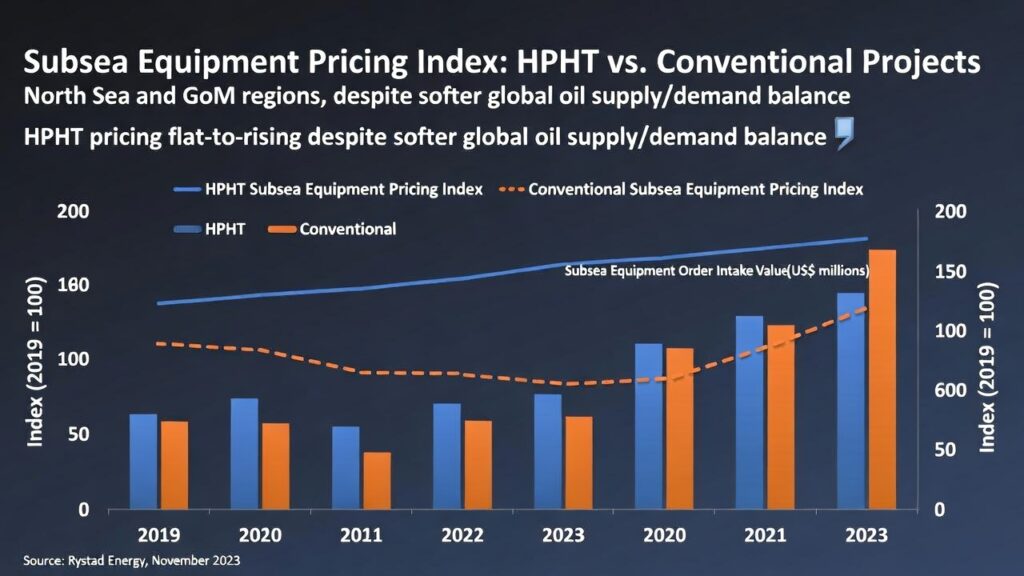

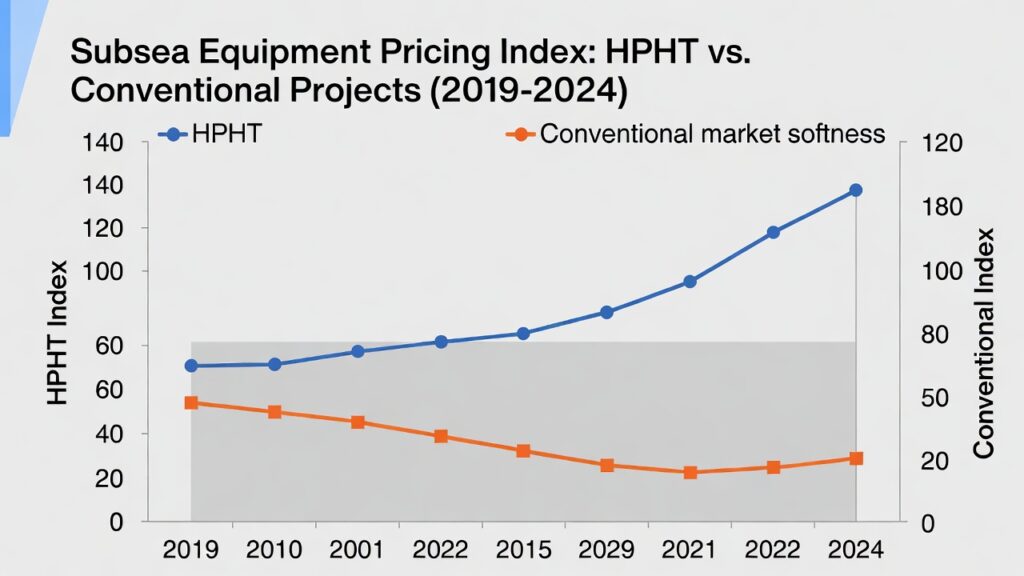

2. Market Dynamics: Oil Supply Outpacing Demand, Yet Subsea HPHT Pricing Holds Strong Global oil markets in early 2026 show supply slightly ahead of demand (IEA/OPEC estimates ~1.0–1.5 MMbpd surplus), driven by non-OPEC growth (U.S. shale, Guyana, Brazil pre-salt). Brent prices hover in the $70–85/bbl range — supportive but not euphoric.Despite this, subsea pricing for complex HPHT developments remains resilient, particularly in the North Sea and Gulf of Mexico.

- Why HPHT pricing holds:

- Limited contractor capacity for 20K-rated equipment (trees, manifolds, flowlines, connectors).

- High barriers to entry proven qualification (I3P, API 17D), fatigue-resistant materials, and long-lead manufacturing.

- Regional demand concentration North Sea (Equinor, TotalEnergies HPHT tiebacks) and GoM (Anchor follow-ons, Kaskida, Shenandoah South) keep order books full.

- Complexity premium HPHT wells require advanced metallurgy, thermal management, and integrity systems that command 30–50% higher costs than conventional subsea.

Figure 2: Subsea Pricing Resilience Index (2024–2026)

( Line/bar chart showing subsea equipment pricing index for HPHT vs. conventional projects in North Sea and GoM. Highlight flat-to-rising HPHT pricing despite softer global oil supply/demand balance.)

3. The Strategic Balancing Act in 2026

Operators are navigating this landscape with a clear hybrid mindset:

- Invest in low-carbon upstream Electrification of subsea production systems, CCS repurposing of depleted reservoirs, methane abatement, and digital twins to reduce emissions intensity.

- Protect cash flow from resilient assets High-margin HPHT developments in proven basins fund the transition.

- Leverage synergies HPHT expertise (materials, fatigue analysis, subsea power) accelerates floating wind and hybrid hubs.

- Prioritize advantaged barrels Focus on long-life, low-cost deepwater projects with strong economics even at $60–70/bbl.

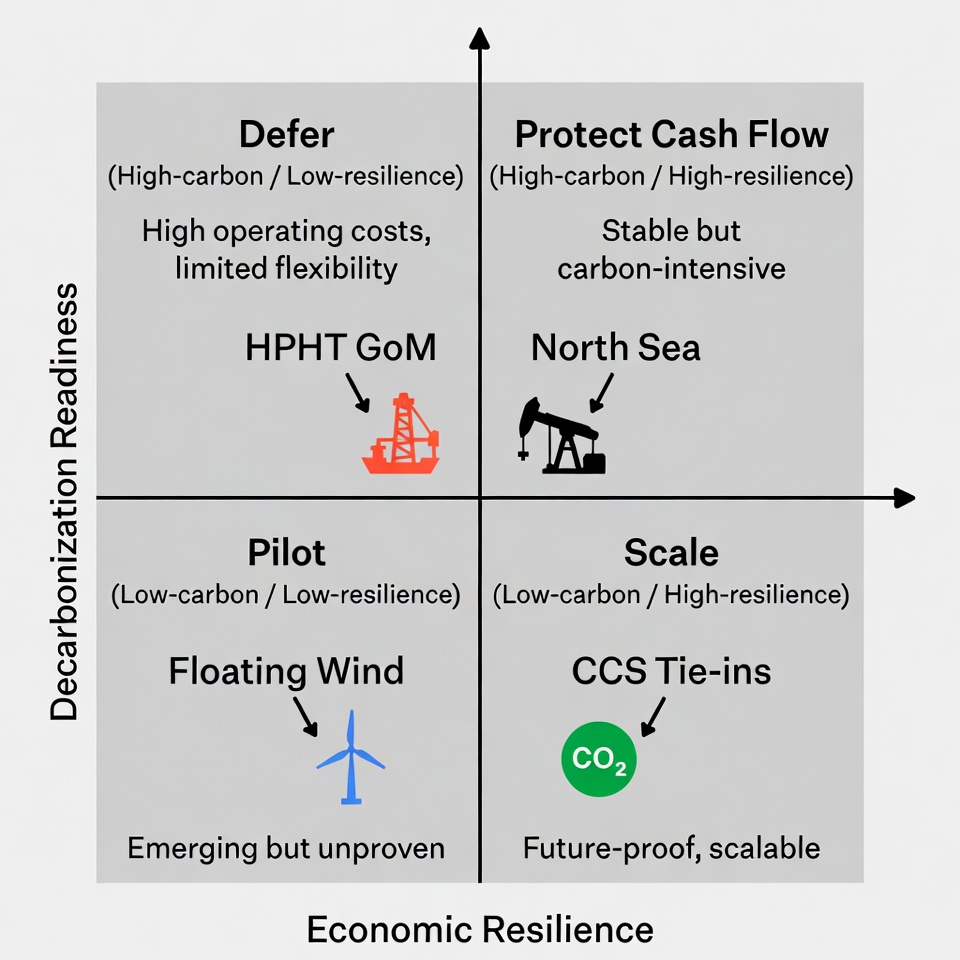

Figure 3: 2026 Offshore Strategy Matrix

( Insert image: 2×2 matrix with axes “Decarbonization Readiness” and “Economic Resilience.” Quadrants labeled: High-carbon / Low-resilience (defer), High-carbon / High-resilience (protect cash flow), Low-carbon / Low-resilience (pilot), Low-carbon / High-resilience (scale). Plot icons for HPHT GoM/North Sea, floating wind, CCS tie-ins.)

The Bottom Line

In 2026, energy security demands both barrels today and a credible path to net-zero tomorrow. Decarbonization is no longer optional it’s fundamental to survival. Yet subsea HPHT pricing remains resilient in key basins, providing the cash flow bridge operators need to invest in the transition.The winners will be those who balance extreme hydrocarbons with smart decarbonization, using digital transformation and cross-industry synergies to stay competitive.

What’s your view is HPHT still the cash cow funding the transition, or are we seeing faster-than-expected wind/CCS economics?

Drop a comment or connect on LinkedIn.Stay sharp out there, brothers. The offshore future is hybrid, resilient, and low-carbon.

Oko Immanuel

Subsea Engineering Specialist | Offshore Pipeline Insight