Published :By Oko Immanuel, M.Eng

05/03/2026.

The offshore pipeline sector is entering a strong growth phase in 2026, with over 113 offshore pipelines scheduled to commence across the globe. Longer tie-backs, LNG export focus, and energy security needs drive many of these mega-projects. Here’s a detailed look at the

top 10 longest pipelines expected to start operations or key commissioning phases in 2026, based on length, capacity, and strategic impact.

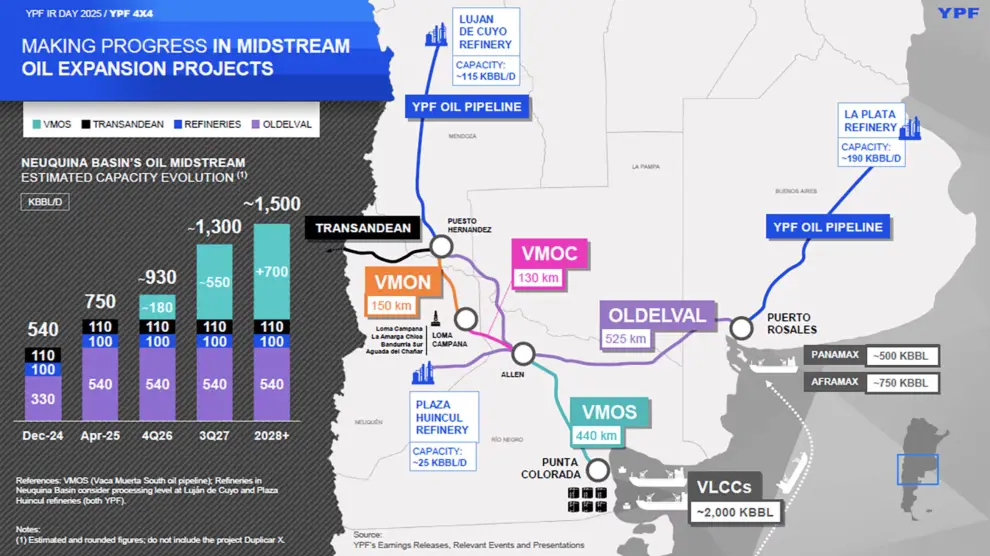

1. Vaca Muerta Sur – Argentina (≈565 km)

Operator: YPF SA

Type: Oil pipeline (onshore + shallow water)

Capacity: ~550,000 barrels/day

Key Details: This flagship project connects the prolific Vaca Muerta shale fields to a new export terminal at Punta Colorada (Golfo San Matias). It features two phases and supports Argentina’s push to become a major oil exporter.

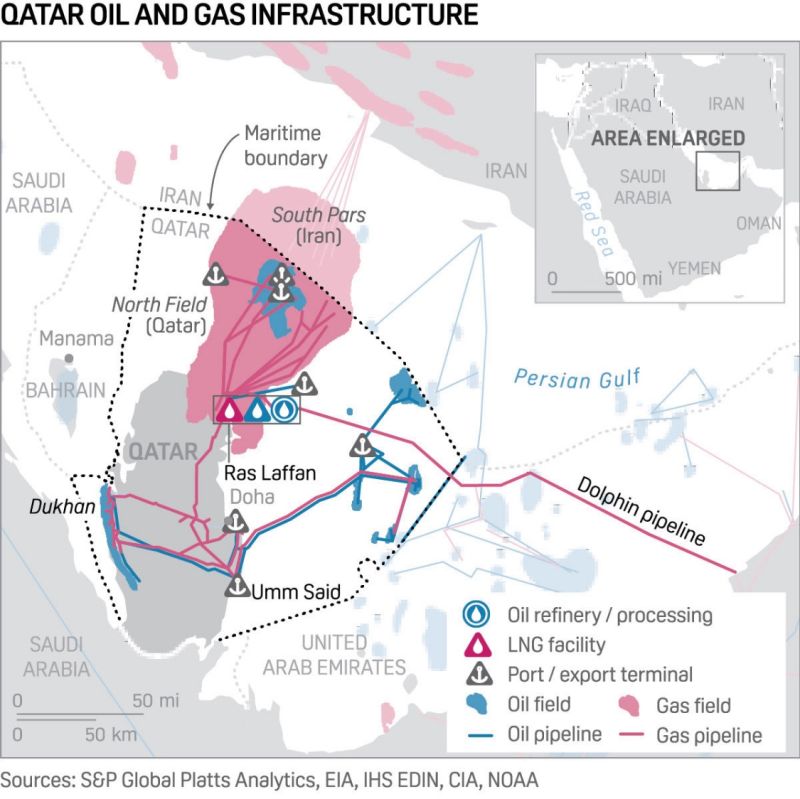

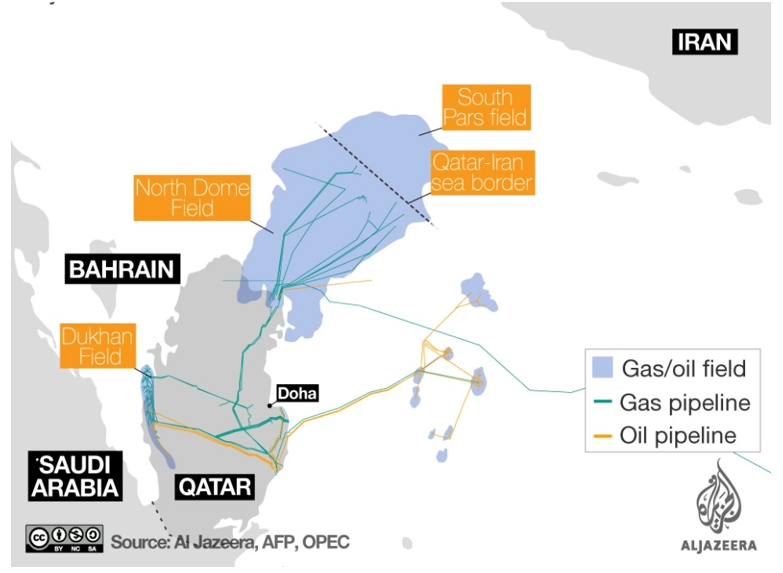

2. North Field East System – Qatar (≈500 km)

Operator: QatarEnergy (with international partners: Shell, ExxonMobil, TotalEnergies, Eni, ConocoPhillips)

Type: Gas pipeline

Impact: Supports the massive North Field expansion, boosting LNG production with integrated carbon capture elements.

Why It Matters:

One of the most ambitious gas infrastructure projects globally, emphasizing sustainability alongside scale.

3. Scarborough–Pluto Pipeline – Australia (≈433 km)

Operator: Woodside Energy

Type: Gas pipeline (deep- to shallow-water)

Capacity: Feeds Pluto Train 2 LNG facility (~8 MTPA)

Status: Construction largely complete; first LNG targeted for Q4 2026.

Technical Note: Traverses varied seabed conditions, requiring advanced materials for HPHT and flow assurance.

4. Block B–O Mon Gas Pipeline – Vietnam (≈433 km)

Operator: PetroVietnam Gas Corporation

Capacity: 656 MMcf/d

Impact: Supplies four gas-fired power plants, boosting domestic energy security in Southeast Asia.

5–10: Other Notable Long Pipelines Starting in 2026

- Rosmari–Marjoram (Malaysia): ~207 km sour-gas pipeline to Bintulu LNG complex.

- Various India ONGC replacement/expansion lines (segments up to 100+ km each, part of larger 1000 km programs).

- Additional Qatar North Field associated lines and Middle East tie-backs.

- Brazil and Gulf of Mexico deepwater tie-backs (typically 50–150 km but high-tech HPHT).

- Southeast Asia and Latin America export lines filling the remaining top 10 slots.

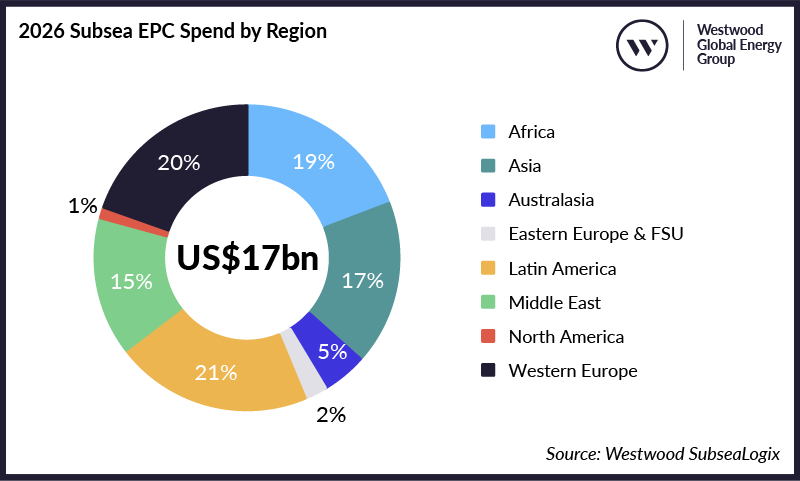

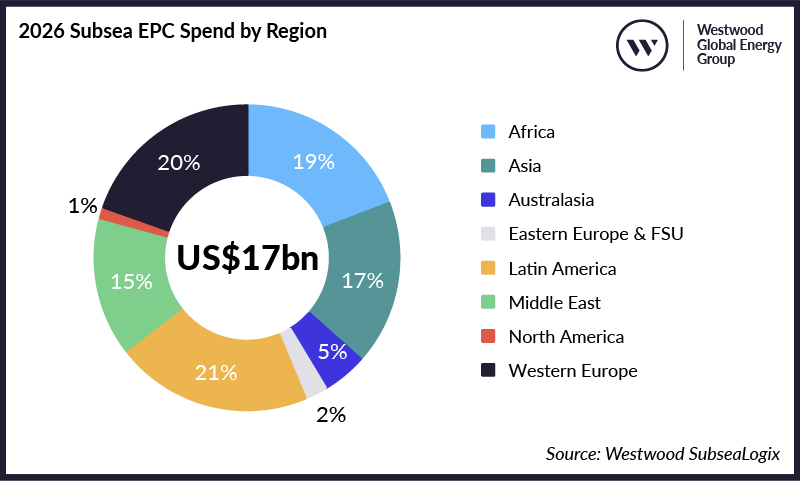

Regional Breakdown of 2026 Offshore Pipeline Activity (approximate by spend/length share):

Key Trends Shaping These Pipelines

- Longer Tie-Backs: Average distances increasing due to frontier developments.

- Materials & Technology: More use of corrosion-resistant alloys (CRA), pipe-in-pipe insulation, and digital monitoring for integrity.

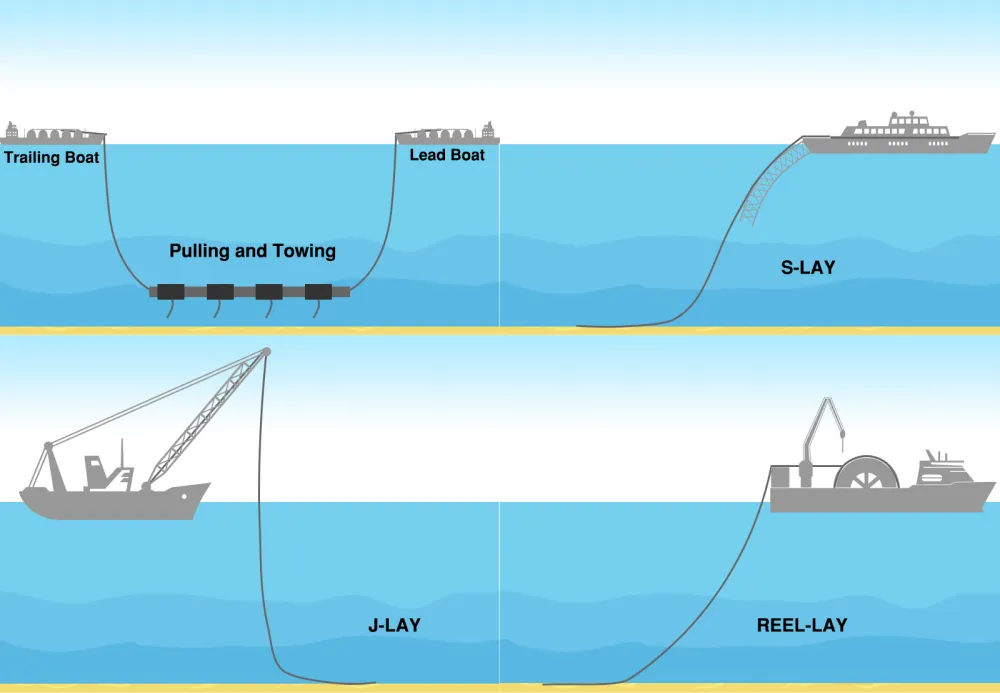

- Installation Methods: Heavy reliance on J-Lay, S-Lay, and reel-lay vessels.

Challenges:

HPHT conditions, deepwater installation risks, regulatory hurdles, and supply chain pressures. Opportunities include local content, decarbonization features, and reuse of existing infrastructure.

This wave of projects underscores a resilient offshore midstream sector amid global energy demands. For subsea engineers, 2026 offers exciting opportunities in design, installation, and integrity management.

By Oko Immanuel, M.Eng

Founder, Offshore Pipeline Insight | Subsea Engineering Specialist Sources include Offshore Technology, project operators, and industry reports (2026 data).