By Oko, Founder of Offshore Pipeline Insight

Published: April 10, 2026

Deepwater and ultra-deepwater developments continue to drive the offshore pipeline sector in 2026. Operators are increasingly relying on subsea tiebacks to existing floating production units (FPUs) and hubs to unlock reserves cost-effectively, while pushing into greater water depths and harsher conditions. The global offshore pipeline market is projected to grow steadily, with the deepwater segment showing one of the fastest CAGRs due to technological advances in materials, vessels, and installation methods.

This article explores the major trends shaping deepwater pipelines in 2026, key technical innovations, persistent challenges, and the resulting implications for midstream and pipeline infrastructure.

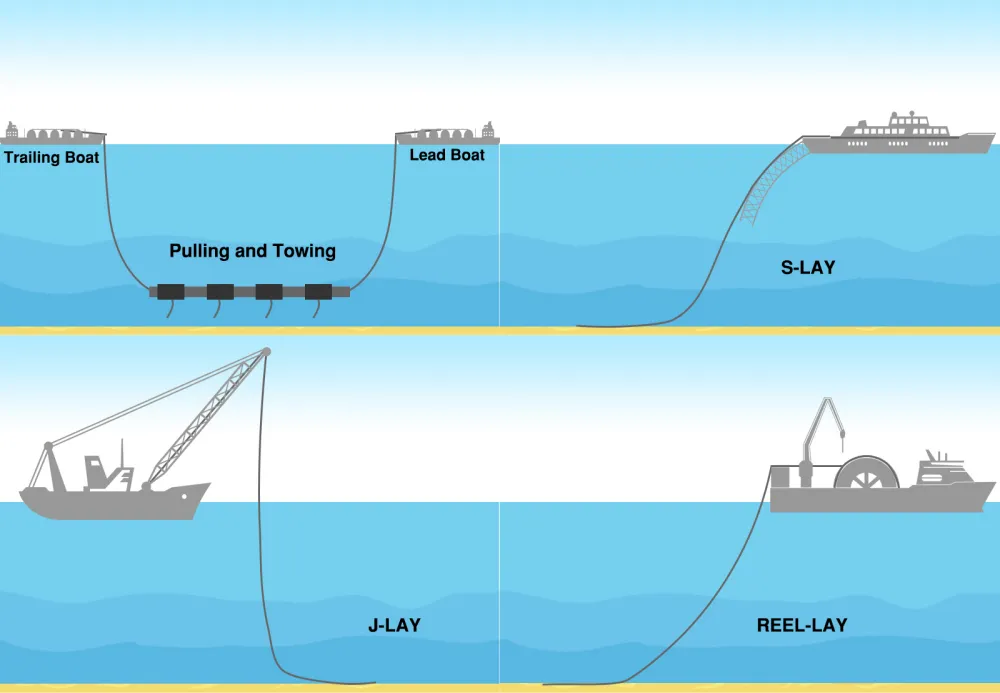

Common offshore pipeline installation methods — S-Lay, J-Lay, and Reel-Lay — are being optimized in 2026 for ultra-deepwater tiebacks and longer distances in challenging seabeds.

Rise of Ultra-Deepwater Tiebacks

Subsea tiebacks remain the dominant strategy for maximizing recovery from existing infrastructure. In the U.S. Gulf of Mexico, multiple tiebacks (including Chevron’s Ballymore, Shell’s Dover, and BP’s Argos Southwest Extension) are boosting production toward record levels near 2.2 million boepd in 2026. Projects like BP’s Kaskida (ultra-deepwater in the Gulf) highlight the move into extreme depths, with wells targeting reservoirs up to six miles below the seabed.

Technical Highlights:

- Longer tieback distances (often 50–100+ km) in water depths exceeding 2,000–3,000 meters.

- High-pressure, high-temperature (HPHT) flowlines requiring robust thermal management and corrosion resistance.

Challenges:

- Extreme pressures and temperatures increase risks of hydrate formation, wax deposition, and material fatigue.

- Geohazards such as steep slopes, seabed currents, and seismic activity demand precise route engineering and on-bottom stability solutions.

Cost-Effective Materials and Design Innovations

Rising steel costs (exacerbated by tariffs) and the need for sour service capability are pushing operators toward smarter material choices:

- Mechanically Lined Pipe (MLP) and weld overlay for large-diameter lines in corrosive environments.

- Clad pipes with corrosion-resistant alloys (CRA) for inner surfaces, offering a balance between performance and cost compared to solid CRA pipes.

- Pipe-in-pipe (PIP) systems with vacuum insulation or advanced coatings for thermal efficiency in cold deepwater conditions (e.g., Norway’s Aasta Hansteen–Irpa project).

These innovations help reduce overall project costs while extending asset life and enabling future repurposing for hydrogen blends or CO₂ transport.

Large-diameter steel pipes prepared for offshore deployment — material selection and cladding innovations are critical for cost control and corrosion resistance in 2026 deepwater projects.

Installation Innovations

Installation remains one of the biggest cost drivers. Key advancements in 2026 include:

- Enhanced J-Lay and Reel-Lay capabilities on modern pipelay vessels for ultra-deepwater efficiency.

- Improved pre-commissioning techniques (e.g., Baker Hughes’ Denizen system) that allow operations at record water depths.

- Greater use of modular and standardized components to accelerate installation and reduce offshore hook-up time.

These methods help mitigate the impact of higher vessel day rates and supply chain pressures.

Midstream and Pipeline Implications

The shift toward deepwater tiebacks and longer flow lines creates both opportunities and challenges for midstream operators:

- Concentrated hubs: Fewer new platforms but higher reliance on existing FPUs means optimized gathering systems and larger trunk lines to handle combined production volumes.

- Takeaway capacity: Initial high production rates from new tiebacks can stress existing export pipelines and terminals, creating short-term bottlenecks but long-term demand for expansions.

- Decarbonization readiness: Many new pipelines are being designed with future flexibility in mind — easier conversion for low-carbon molecules or integration with CCUS networks.

- Cost pressures: Steel tariffs and material inflation are encouraging repurposing of existing infrastructure rather than greenfield builds, accelerating hybrid hydrocarbon/low-carbon strategies.

Overall, 2026 deepwater pipeline activity reinforces a more efficient, tieback-heavy development model that extends the life of mature basins while unlocking frontier reserves.

What deepwater pipeline trends or specific projects are you watching most closely in 2026?

How do rising material costs and installation innovations affect your midstream planning?