Macro Energy Transitions & Co-Location Series – Topic 1: The Data Center Power Crisis

By Oko Immanuel, M.Eng | Offshore Pipeline Insight | June 2026

The AI revolution is devouring electricity at an unprecedented pace. Data centers, the physical backbone of artificial intelligence, are no longer niche infrastructure—they are industrial-scale power hogs reshaping global energy markets. Tech giants once heralded a future powered purely by renewables. Reality has forced a pragmatic truce: a hybrid reality where wind farms in Texas dance alongside new natural gas plants, and hyperscalers quietly secure reliable baseload power to keep servers humming 24/7.

This article explores the data center power crisis in depth, the surprising alliance between fossil fuels and renewables, and what it means for energy transitions, grid reliability, and the future of AI infrastructure.

The Scale of the Beast: AI’s Electricity Appetite

Global data center electricity consumption stood around 460–485 TWh in 2024–2025, roughly 1.5–2% of worldwide electricity use. Projections show this roughly doubling to 945–1,050 TWh by 2030, potentially reaching 3% or more of global demand. AI-focused data centers are growing even faster—tripling in consumption over the same period.

In the United States, data centers consumed about 4.4% of total electricity in 2023 (around 176 TWh). By 2028, estimates range from 6.7% to 12% (325–580 TWh). Standalone data centers and AI workloads drive much of this surge. Servers alone could account for 7% of commercial sector electricity in 2025, rising dramatically by 2050. A single large AI data center campus can demand hundreds of megawatts—equivalent to powering a mid-sized city. Training frontier models requires gigawatt-hours, while inference (everyday AI queries) now dominates and grows at ~30% annually. One advanced query might use 10x the energy of a traditional search.

Why the spike?

- Explosive growth in GPU/accelerator clusters (NVIDIA-driven).

- Hyperscalers (Microsoft, Google, Amazon, Meta, Oracle) pouring hundreds of billions into capex—over $400 billion in 2025 alone.

- AI model scaling laws favoring bigger, always-on compute.

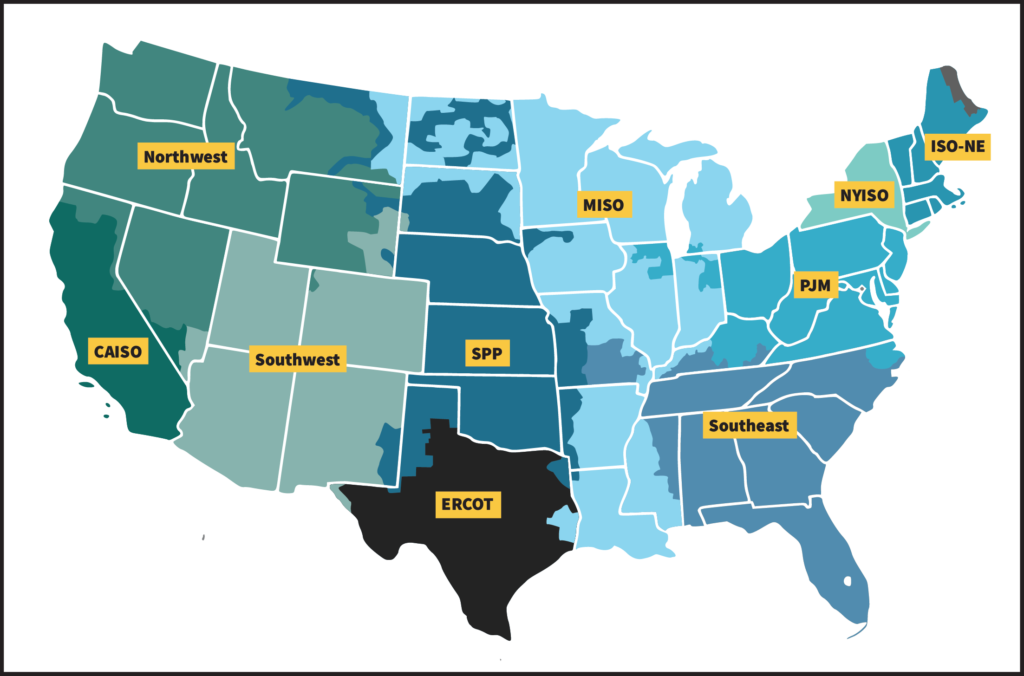

This isn’t abstract. In PJM (mid-Atlantic grid), data centers contributed ~40% of recent capacity auction costs. In ERCOT (Texas), large load queues (mostly data centers) jumped nearly 300%, exceeding 230 GW in requests.

Grid Strain and the Reliability Imperative

Data centers require 24/7 base-load power with near-perfect uptime. Renewables like wind and solar are intermittent—excellent for marginal clean electrons but insufficient alone for always-on AI factories without massive storage (which remains expensive and limited).

Grid interconnection queues are backlogged for years. Transformer and equipment shortages add delays. In hotspots like Northern Virginia (PJM) and Texas (ERCOT), utilities face unprecedented load growth. Some projects face 5+ year waits. This forces pragmatism:

In ERCOT (Texas): Wind-rich but with strong gas infrastructure. Texas leads U.S. data center growth thanks to fast permitting, abundant land, and flexible generation. Gas projects now outpace wind in interconnection queues for the first time in years, driven by data center demand. Over 40 GW of gas generation in development.

Tech giants are co-locating or building behind-the-meter power. Examples include Google’s partnerships, Energy Transfer supplying gas to Cloud Burst/Fermi America HyperGrid (11 GW mixed project with gas, nuclear, solar, wind), and Pacifico Energy’s GW Ranch (up to 7.7 GW gas for private grid). In PJM: Data centers drive capacity prices sky-high. Auctions saw billions added to costs, passed partly to consumers. Proposals include data centers self-supplying power (often gas) for faster permitting.

The Truce: Renewables + Gas in Action

Tech companies maintain 24/7 carbon-free energy (24/7 CFE) goals, but timelines slip. Many now prioritize reliable power over pure green credentials in the short term.

- Wind in Texas: ERCOT has massive wind capacity. Data centers in West Texas tap curtailment-prone wind via PPAs. Google’s $40B Texas expansion targets wind-rich zones.

- Gas as Bridge: Natural gas provides dispatchable power. New combined-cycle and simple-cycle plants, on-site generation, and direct pipeline deals fill gaps. Vistra, Energy Transfer, and others expand. Some “peaker” plants revived.

Case Studies: Hyperscalers Adapting

Microsoft, Google, Amazon, Meta, Oracle: Billions committed. Google plans gas for some Texas sites while expanding wind PPAs. Microsoft explores small modular reactors (SMRs) and gas. Oracle’s Stargate project includes on-site generation.

Many sign renewable PPAs but back them with gas or batteries for firmness. Some delay projects or pay premiums for priority power.

Consumer Impact: Higher capacity costs in PJM/ERCOT translate to rising bills. Virginia data centers already ~40% of state consumption. Ratepayers worry about subsidizing tech giants.

Broader Implications for Energy Transitions

This truce challenges pure decarbonization narratives but accelerates overall generation buildout. Positives:

- Massive investment in grids, transmission, and diverse generation.

- Innovation in cooling (liquid, immersion), efficiency, and behind-the-meter tech.

- Potential nuclear revival (SMRs for baseload).

Challenges:

- Short-term emissions uptick if gas/coal fills gaps.

- Grid modernization urgency.

- Equity: Who pays for upgrades?

Long-term, AI efficiency gains (better chips, algorithms) and storage could tilt back toward higher renewables. But near-term realism prevails: Power density and reliability trump ideology.

What Comes Next?

Strategies for the Industry

- Hybrid Power Architectures: Renewables + gas + storage + emerging nuclear.

- Policy Support: Faster permitting, co-location incentives, cost allocation that doesn’t burden residential users.

- Tech Innovation: Advanced cooling, chip efficiency, demand response (flexible workloads).

- Offshore & Pipeline Synergies: Subsea cables, hydrogen, or floating data centers? (Relevant to our offshore focus—watch for energy transport innovations.)

- Investment Opportunities: Gas midstream, transmission, nuclear supply chain, specialized pipelines for fuel delivery.

For offshore pipeline professionals: Data center-driven gas demand boosts LNG, pipeline projects, and potentially CCUS integration for lower-carbon gas power.

Conclusion: Pragmatism Powers Progress

AI data centers are forcing energy markets into a mature, hybrid phase. The “truce” between wind-rich grids and natural gas isn’t a setback—it’s an engineering necessity enabling the AI boom while infrastructure catches up. Tech giants, utilities, and regulators are learning that reliable power comes from diverse, resilient systems, not single-source idealism.

The beast is hungry. Feeding it sustainably and reliably will define energy transitions for the 2030s. Expect more co-location, hybrid projects, and pragmatic policy. For those in pipelines, offshore, and energy infrastructure: this is your moment—AI’s power needs are creating pipelines of opportunity, literally and figuratively.

What’s your take, readers? Share in comments—especially if you’re in data center siting, grid planning, or pipeline development.

Next in series: Co-Location Deep Dive – Gas, Nuclear & Renewables Side-by-Side.

Sources include IEA, EIA, LBNL, Goldman Sachs, ERCOT/PJM reports, and industry announcements (2025–2026). Data as of mid-2026.