Oil & Gas Market Update – June 2026

By Oko, M.Eng | Offshore Pipeline Insight

Global oil markets remain in a delicate balance in mid-2026. Inventories are tighter than normal due to earlier geopolitical disruptions, while OPEC+ is gradually unwinding production cuts. Demand growth is modest but steady, and non-OPEC supply — particularly from the US, Brazil, and Guyana — continues to expand.

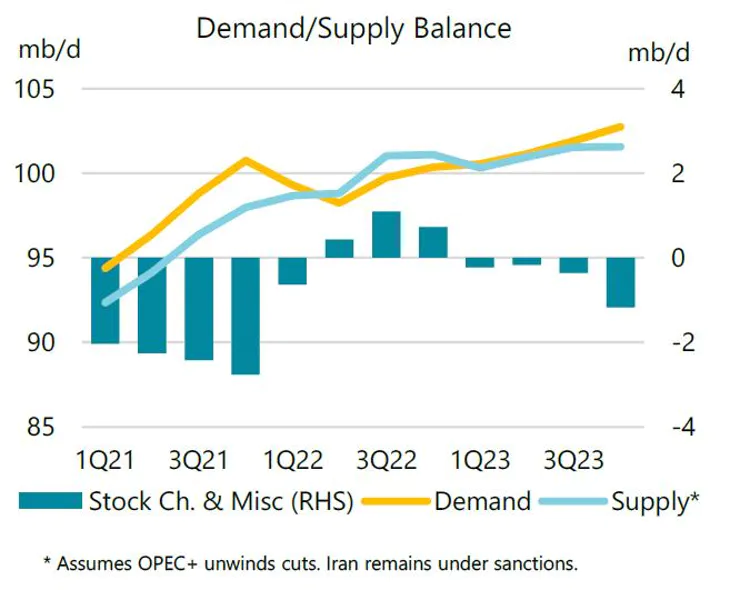

Current Supply SituationGlobal inventories

are still relatively tight following the 2026 disruptions in the Strait of Hormuz and related Middle East tensions. However, the recent US-Iran ceasefire has allowed some supply recovery to flow back into the market.OPEC+ is slowly bringing barrels back online:

- Voluntary cuts are being unwound in a measured way.

- This gradual return is helping to ease tightness but is also contributing to the recent price pullback.

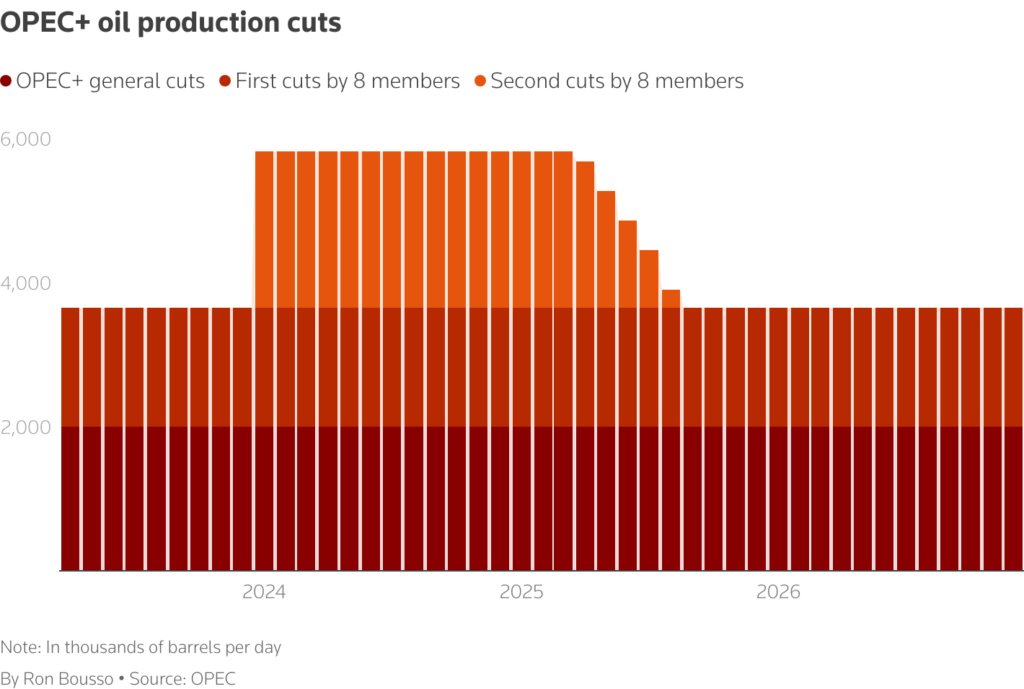

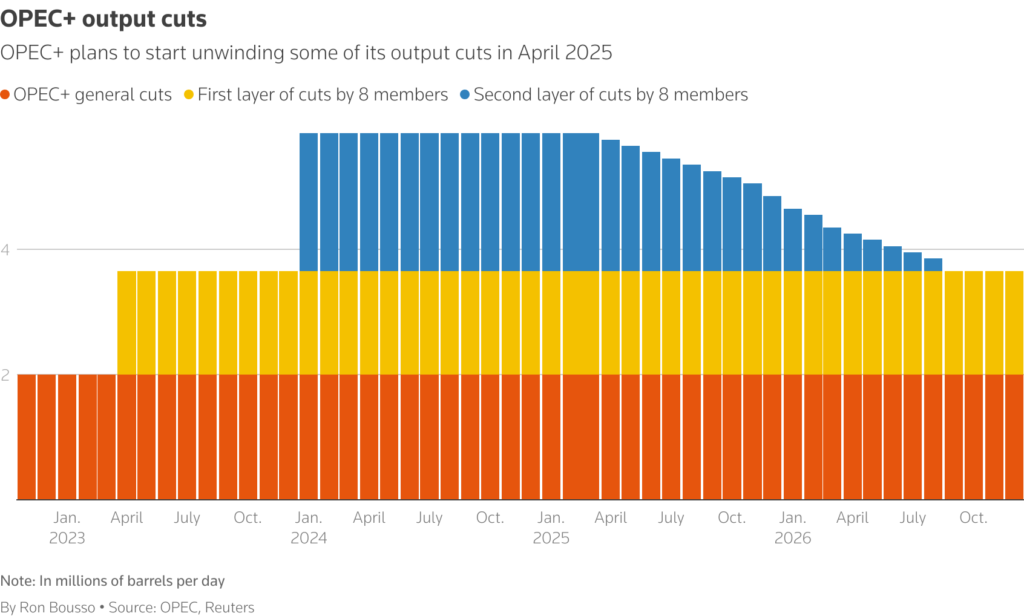

Caption: OPEC+ production cuts timeline — showing the gradual unwinding phase in 2026.

Demand Growth: Modest but Asia-Driven

Global oil demand growth for 2026 is forecast at approximately 1.0–1.4 million barrels per day (mb/d).

Key Drivers:

- Asia leads — Strong growth from China (stockpiling) and India (rising industrial and transportation needs).

- Petrochemicals remain a major support.

- Headwinds: High prices and economic uncertainty are tempering demand in OECD countries.

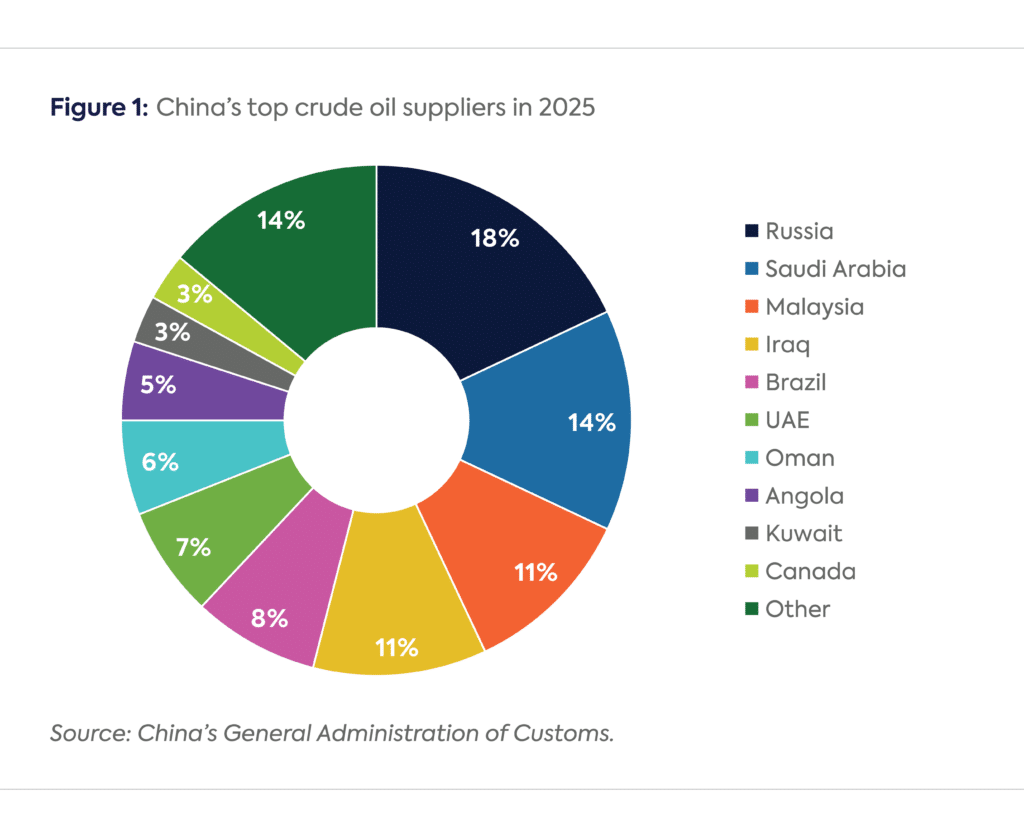

Caption: China’s top crude oil suppliers in 2025–2026 — highlighting Asia’s dominant role in global demand.Supply Side Strength: Non-OPEC Growth

Non-OPEC supply is delivering robust growth in 2026:

- US Shale — Continues to add volumes despite efficiency gains and capital discipline.

- Brazil Pre-Salt — Multiple new FPSOs coming online.

- Guyana — ExxonMobil’s Stabroek Block projects (Uaru, Whiptail) pushing toward 1.4+ million bpd.

- Other Offshore — Namibia, Suriname, and new projects in Southeast Asia.

This strong non-OPEC growth creates potential oversupply risks in 2027 if OPEC+ continues unwinding cuts and production fully normalizes.

Caption: Offshore platforms in Brazil pre-salt and Guyana — key sources of new supply growth in 2026.

What This Means for Offshore & Pipeline Professionals

- Tieback Opportunities: At current price levels, fast-payback subsea tiebacks remain highly attractive.

- LNG & Gas Projects: Steady demand supports continued investment in gas infrastructure and subsea pipelines.

- Project Timing: Operators are prioritizing projects with flexible economics that can handle price swings.

- Longer-Term Risk: If oversupply materializes in 2027, marginal offshore developments could face delays or deferrals.

The market is currently balanced but watchful. Tight inventories provide a floor, while strong non-OPEC supply and gradual OPEC+ unwinding create a ceiling.