By Oko,M.Eng / 05/04/2026

Founder, Offshore Pipeline Insight | Subsea Engineering Specialist

Analysis based on 2026 market data, EIA, IEA, and real-time shipping intelligence.

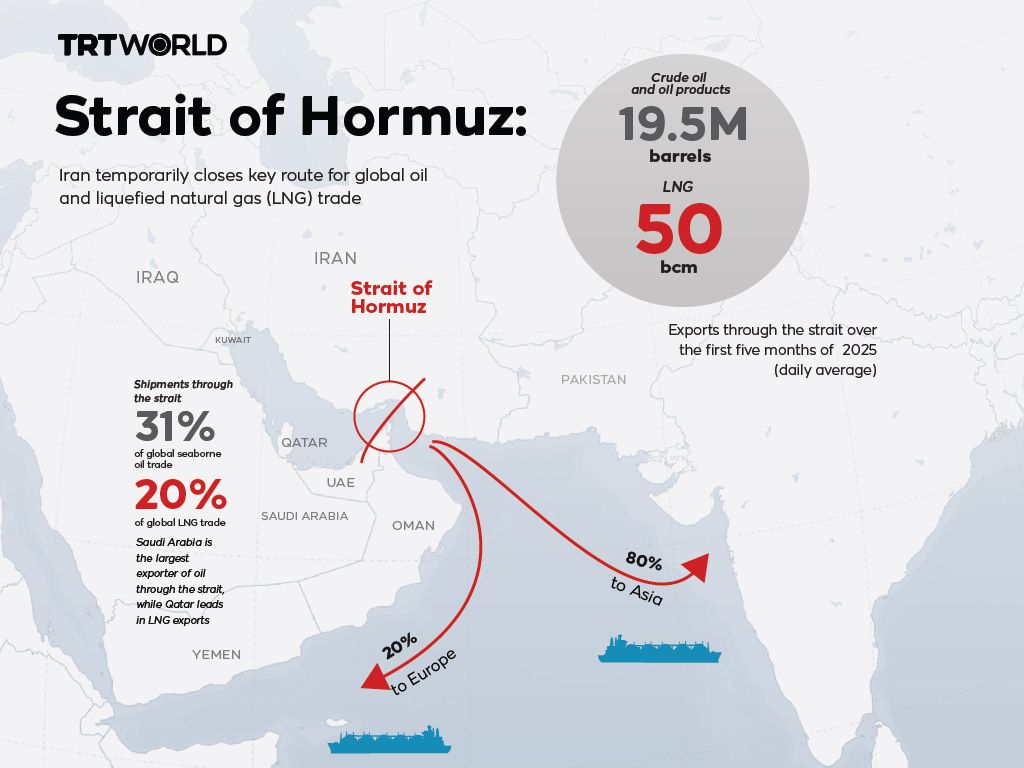

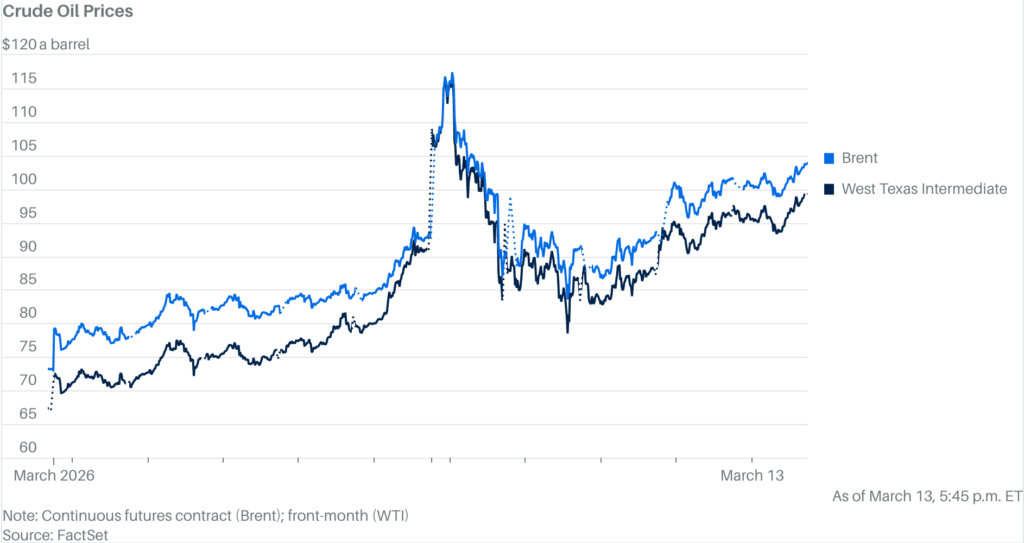

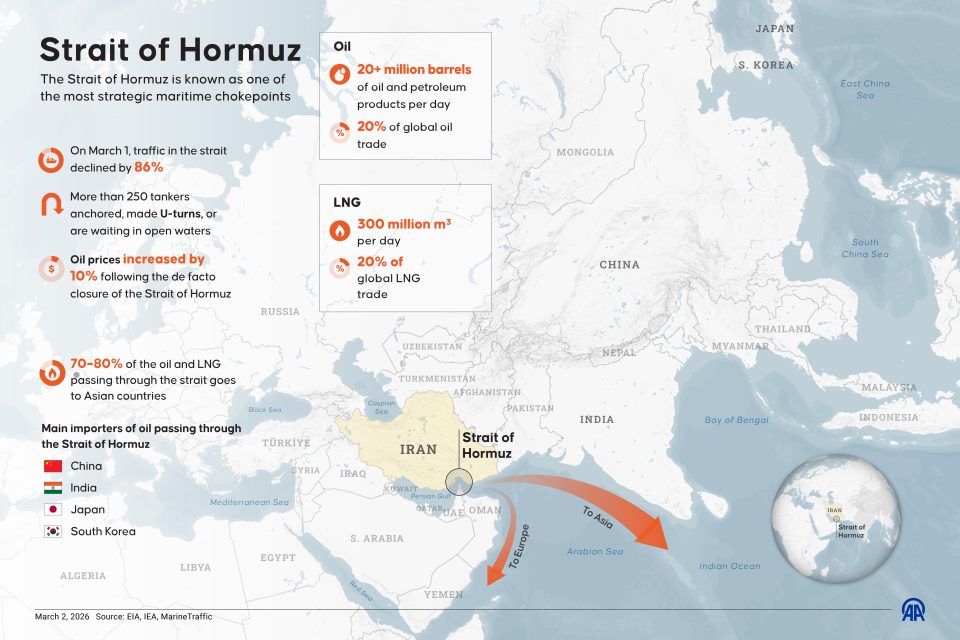

The Strait of Hormuz — a narrow 33 km-wide waterway between Iran and Oman — has long been the world’s most critical energy chokepoint. In early 2026, geopolitical tensions escalated into a temporary closure, halting roughly 20–21% of global seaborne oil trade and 20% of LNG shipments. The immediate result: Brent crude surged above $115 per barrel, sending shockwaves through global markets.

Understanding the Hormuz Factor

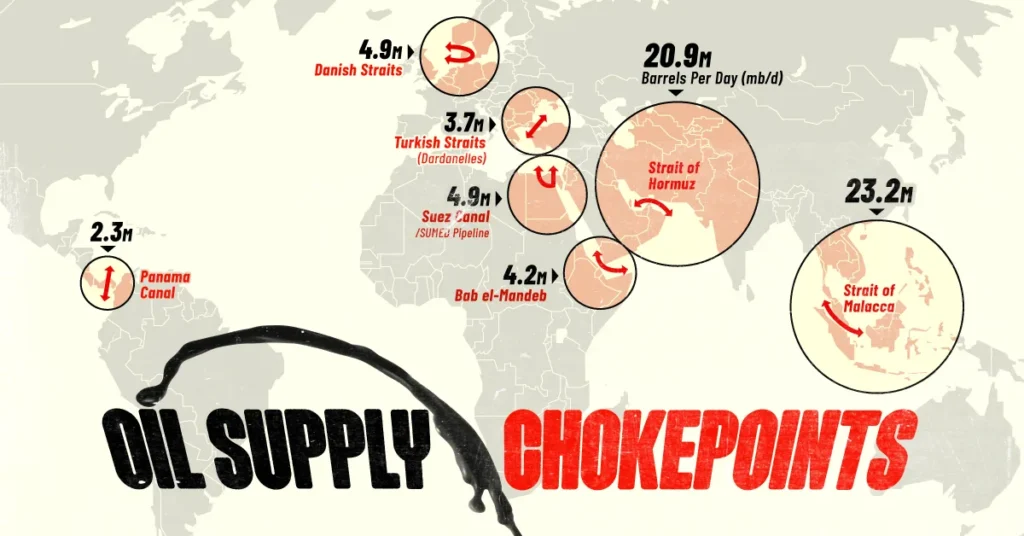

The Hormuz Factor refers to the systemic risk posed by over-reliance on this single maritime corridor. Every day, approximately 21 million barrels of oil and 300 million cubic meters of LNG pass through it — volumes that cannot be easily replaced in the short term.When the strait closed in March 2026 (due to heightened regional conflict), the world discovered how fragile modern energy logistics truly are. Tanker traffic dropped by up to 86% in days, forcing hundreds of vessels to anchor or divert.

The $115 Oil Peak and Immediate Market Impact

The price surge to $115/barrel was not speculation — it was mathematics. With ~19.5 million barrels per day of crude and products suddenly offline, global inventories drew down rapidly. Brent futures spiked over 55% in under two weeks.This was not just an oil story:

- LNG prices in Asia jumped 40–60%.

- Shipping rates for alternative routes (around the Cape of Good Hope) more than doubled.

- Chemical and polymer feedstocks (tied to oil) caused downstream inflation in plastics, fertilizers, and manufacturing.

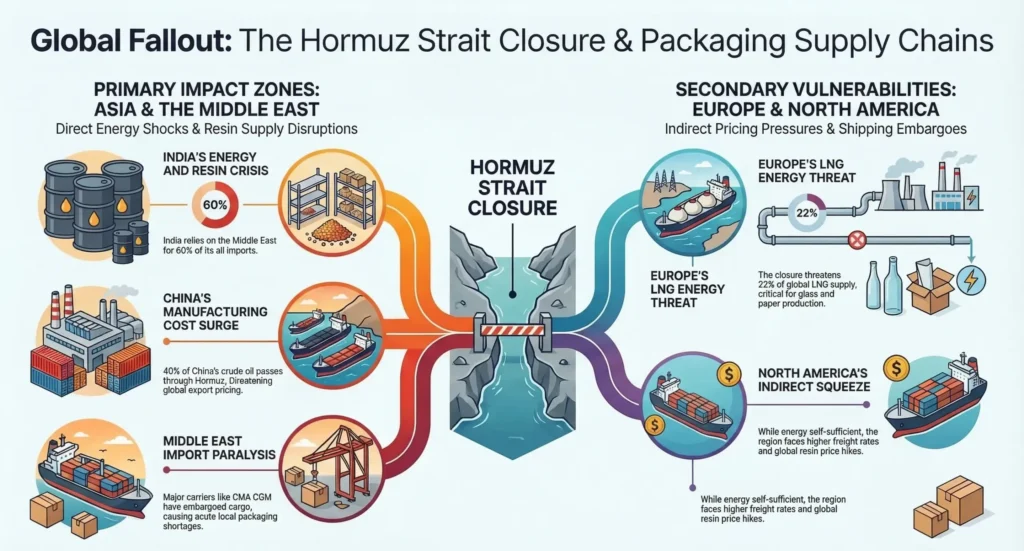

Global Supply Chain Disruption: Beyond Oil

The closure revealed how interconnected modern supply chains are with Middle East energy:

- Asia (China, India, Japan, South Korea) — which imports 70–80% of its oil via Hormuz — faced immediate shortages and rationing.

- Europe saw LNG diversions and higher power prices.

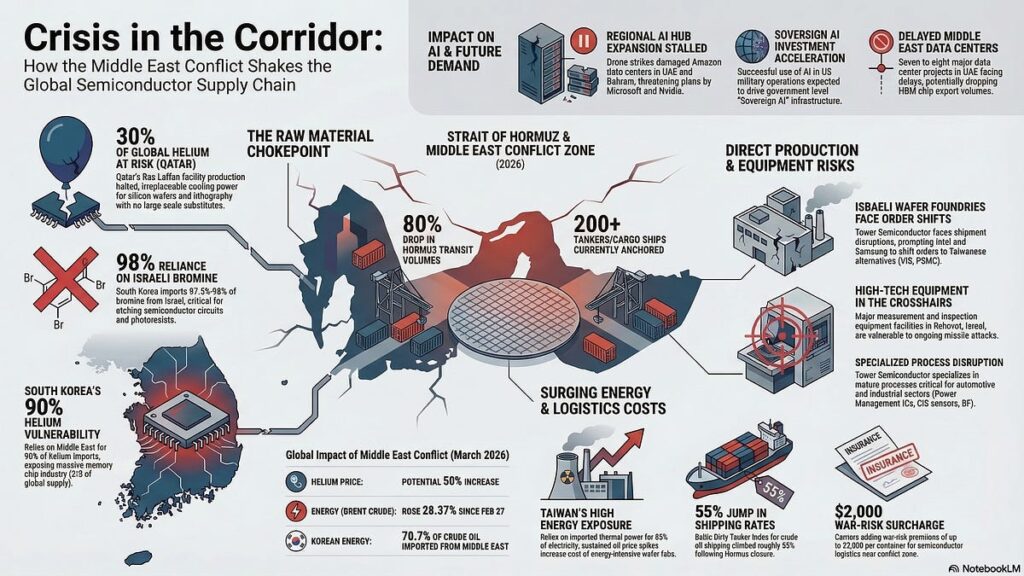

- Manufacturing sectors (semiconductors, petrochemicals, packaging) suffered raw material and energy cost spikes.

Energy Security Rethink: The New Strategic Priority

Governments and corporations are now treating energy security as a national security imperative, not just a cost issue.

Key shifts include:

- Diversification of Supply Routes

Massive acceleration of bypass pipelines and overland options. - Strategic Reserves and Stockpiling

Countries are expanding SPRs (Strategic Petroleum Reserves) and building new floating storage. - Acceleration of Renewables + Nuclear

To reduce oil dependence long-term. - Subsea and Offshore Infrastructure Resilience

This is where subsea engineers play a critical role.

Direct Implications for Offshore Pipelines and Subsea Systems

The Hormuz crisis has direct consequences for the offshore and subsea sector:

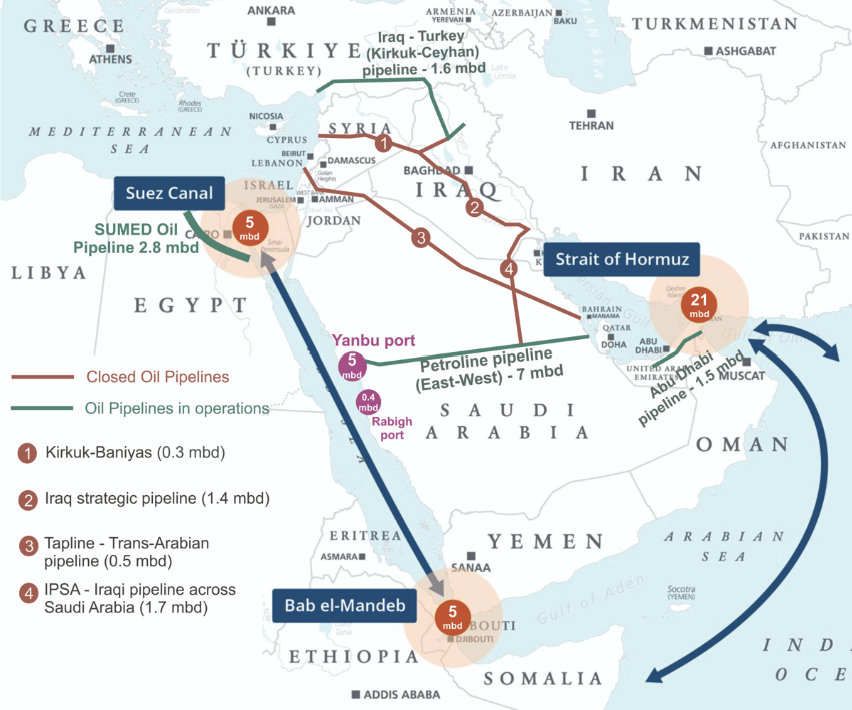

- Middle East Pipelines Under Pressure: Operators in the Persian Gulf are fast-tracking new subsea tie-backs and export lines that avoid surface tanker reliance.

- LNG Export Infrastructure Boom: Qatar, UAE, and Oman are expanding subsea power distribution and all-electric systems to support larger liquefaction trains.

- New Bypass Routes: Projects like the Habshan–Fujairah pipeline and East–West Petroline are being expanded, while new subsea concepts for direct-to-shore gas export are under study.

- HPHT and Deepwater Resilience: Fields in deeper waters (e.g., pre-salt analogs or GoM-style developments) gain strategic value because they are less exposed to chokepoint risks.

- Supply Chain for Subsea Equipment: Higher oil prices improve project economics for new subsea tie-backs in safer basins (Guyana, Brazil, North Sea, West Africa).

Strategic Adaptation Roadmap for 2026 and BeyondThe industry is responding with three clear pillars:

| Adaptation Strategy | Timeline | Subsea/Offshore Impact | Expected Outcome |

|---|---|---|---|

| Pipeline Diversification | 2026–2028 | New subsea export lines & bypass pipelines | Reduced tanker dependence |

| LNG Fleet & Terminal Expansion | 2026–2029 | More subsea power & control systems for terminals | Faster LNG export capacity |

| Digital Twins & Resilience Modeling | Immediate | AI-driven monitoring of critical subsea assets | Faster response to disruptions |

| Hybrid Energy Hubs | 2027+ | Integration of offshore wind with oil/gas platforms | Lower emissions + energy security |

The Bottom Line for Subsea Engineers and Pipeline Professionals

The Hormuz Factor has permanently changed the risk equation. Projects that were marginal at $70 oil are now highly attractive at sustained $90–110 levels. Longer tie-backs, all-electric subsea systems, and robust flow assurance solutions are no longer “nice-to-have” — they are essential for energy security.For those of us in the subsea and offshore pipeline space, 2026 marks the beginning of a new era: one where technical excellence in HPHT design, subsea power distribution, and integrity management directly supports global stability.

The closure was a shock. The $115 peak was painful. But the resulting rethink may prove to be the most important catalyst for a more resilient global energy system in decades.

By Oko Immanuel, M.Eng

Founder, Offshore Pipeline Insight | Subsea Engineering Specialist

Analysis based on 2026 market data, EIA, IEA, and real-time shipping intelligence.