The Deepwater “Black Gold Rush” (Offshore)

By Oko, M.Eng | Offshore Pipeline Insight | June 2026

While U.S. shale hype dominated the last decade, 2026 marks a decisive pivot. International capital is flooding into massive deepwater and ultra-deepwater mega-projects across Africa, South America, and Southeast Asia. Operators are chasing lower breakeven costs, giant resource scales, and long-life reserves that onshore shale struggles to match.

This article maps the new global oil frontier — why deepwater is winning the capital allocation war.

The Economics: Deepwater vs. Shale Breakevens

Offshore deepwater projects now deliver some of the most competitive breakevens in the industry.

- Deepwater / Ultra-Deepwater: ~$35–$45/bbl (many projects below $40/bbl all-in).

- New U.S. Shale (Permian, etc.): ~$60–$70/bbl for new wells, with marginal inventory climbing toward $95/bbl by the mid-2030s.

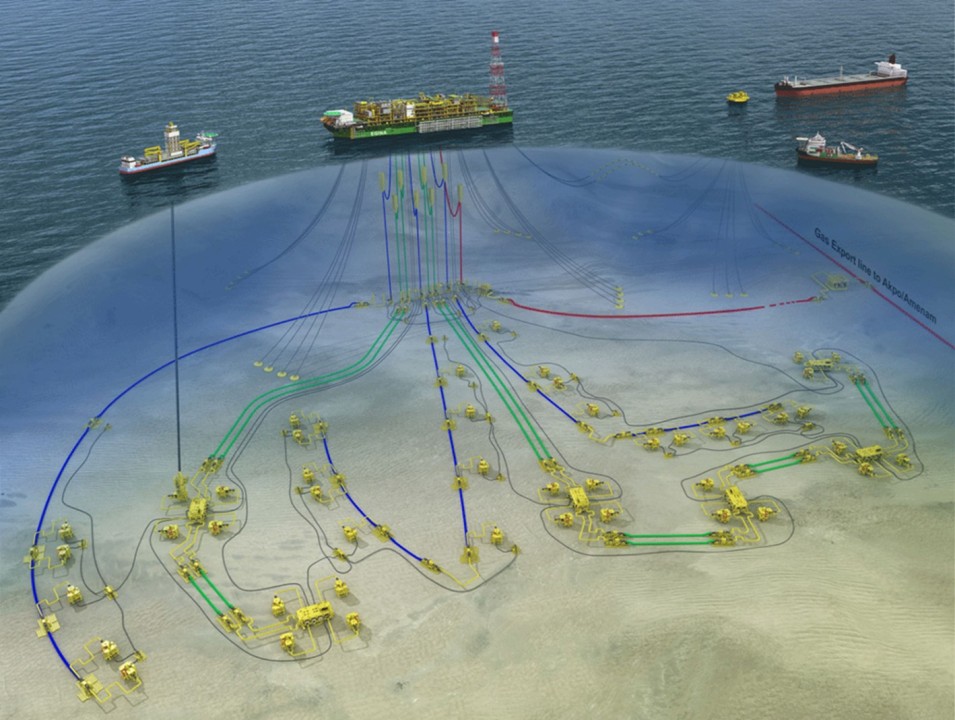

Deepwater wins because of massive scale per well, high initial production rates, and long plateau periods (often 10–20+ years). Once online, FPSOs and subsea tie-backs generate strong free cash flow even at moderate oil prices.

Namibia: Africa’s Emerging Deepwater Hotspot

Namibia’s Orange Basin has become one of the most exciting frontiers.

- Shell’s recent Merlin-1X well delivered strong results.

- TotalEnergies’ Venus project targets FID in late 2026.

- Galp’s Mopane discovery holds up to 10 billion barrels potential.

Guyana: The Stabroek Block Machine

ExxonMobil’s Stabroek Block continues its world-class run:

- Uaru (fifth project) on track for startup in 2026 — ~250,000 bpd.

- Production heading toward 1.4 million bpd+ across multiple FPSOs.

Brazil Pre-Salt: The FPSO Factory

Brazil’s pre-salt continues setting records with dozens of high-capacity FPSOs (many 150,000–225,000 bpd) in Búzios, Mero, and other giants. Petrobras plans 11+ new FPSOs by 2027–2030.

Indonesia: Eni’s $15 Billion King North / Geng North Hub

Eni is advancing a major gas-condensate development in the Kutei Basin with ~$15 billion investment and new FPSO.

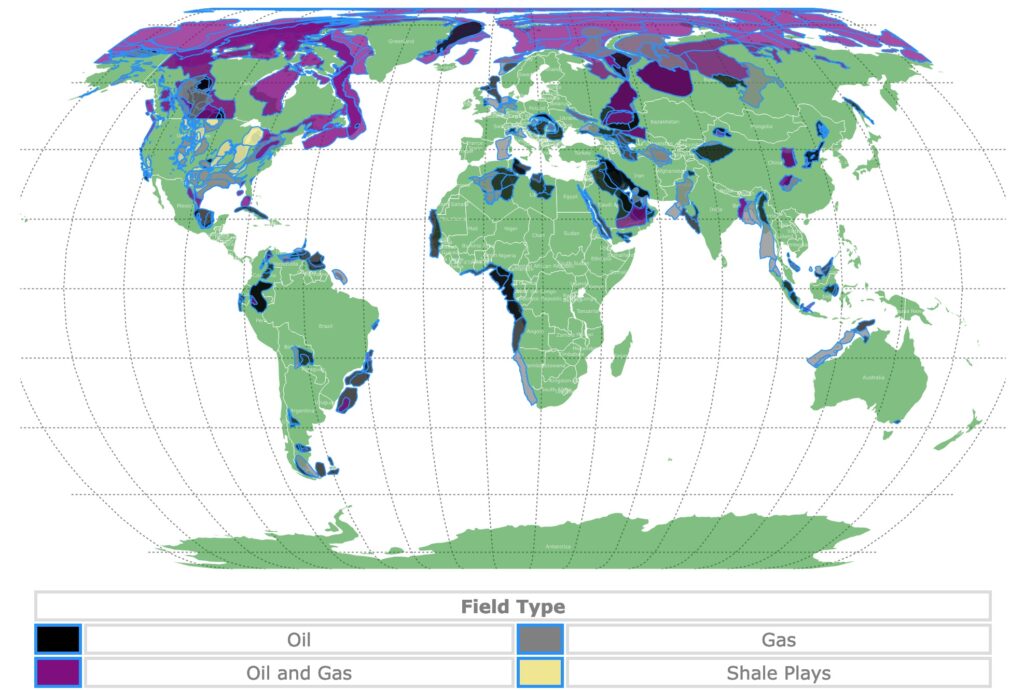

Global View: The Shifting Oil Map

Why the Capital Pivot is Happening Now

- Superior full-cycle returns and decades-long production.

- Massive resource scale per discovery.

- Technology maturity (FPSO standardization, subsea tie-backs).

- Portfolio diversification for majors.

Implications for Offshore Pipeline & Subsea Professionals

This resurgence drives strong demand for new flow-lines, risers, umbilicals, export pipelines, and subsea infrastructure — plus opportunities in CCUS integration and hydrogen-ready systems.

The New Map of Global Oil

The 2026 map highlights deepwater hotspots in Namibia, Guyana, Brazil, Indonesia, and beyond. Deepwater isn’t just surviving — it’s thriving as the premier growth engine for international oil supply.

What’s your view on the deepwater resurgence? Are you working on any of these projects?

Share in the comments! Next in the series: Floating Wind + CCUS Hubs.

Sources: Shell, ExxonMobil, Petrobras, Eni, TotalEnergies, Rystad, WoodMac (2025–mid-2026 data).

Amazon Associate Note

This website contains Amazon affiliate links. If you click on any of these links and make a purchase you have help the website. https://amzn.to/4gpqMQ3

Thank you for supporting Offshore Pipeline Insight.