The global offshore pipeline sector is entering one of its busiest years on record. With 113 offshore pipelines scheduled to come online in 2026 and total pipeline project value exceeding $85 billion, securing the right financing has never been more critical — or more challenging.

Operators face higher interest rates, stricter ESG lending rules, volatile oil prices, and the added complexity of energy transition projects (CCUS, hydrogen blending, and repurposing). Traditional bank loans alone can no longer cover the scale. This article breaks down exactly how major players are financing 2026’s mega-projects, the innovative structures being used, real-world case studies, and what it means for subsea and pipeline professionals.

Why Financing Has Become So Complex in 2026Several converging factors have changed the game:

- Capital Discipline: Majors continue to prioritize free cash flow and shareholder returns over aggressive volume growth.

- Higher Cost of Capital: Interest rates remain elevated, making pure debt financing more expensive.

- ESG and Transition Pressure: Lenders now demand clear decarbonization plans, especially for new pipelines or repurposing projects.

- Project Scale: Many 2026 developments involve ultra-deepwater tie-backs, long export lines, and multi-billion-dollar infrastructure.

As a result, project finance has shifted toward blended structures that combine bank debt, export credit agencies (ECAs), private equity, infrastructure funds, green bonds, and even government-backed transition funds.

Main Financing Structures Used for 2026 Megaprojects

- Limited Recourse Project Finance

Still the most common for large greenfield pipelines. Debt is repaid from project cash flows only. - Export Credit Agency (ECA) Support

Agencies like US EXIM, UK Export Finance, and SACE (Italy) are heavily involved in projects with significant equipment or engineering from their countries. - Private Equity & Infrastructure Funds

Funds such as Blackstone, Brookfield, and Macquarie are increasingly taking equity stakes in midstream and subsea assets. - Green and Sustainability-Linked Bonds/Loans

Especially popular for pipelines tied to CCUS or hydrogen transport. - Hybrid Blended Finance

Combining commercial debt + development bank money + equity for transition projects.

Real-World Case Studies – How 2026 Projects Are Being Funded

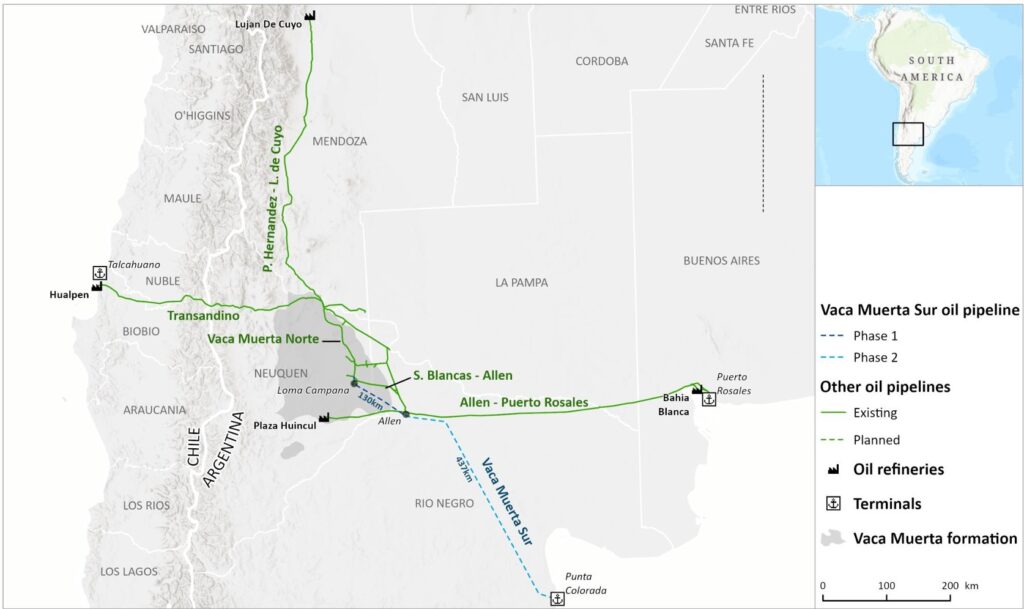

1. Argentina – Vaca Muerta Sur Pipeline (565 km)

One of the largest oil pipeline projects of the year. Total estimated cost: ~$2.2 billion.

Financing structure:

- 60% covered by a consortium of international banks led by JPMorgan and Santander.

- 25% from Argentine development bank BNA and export credit support.

- 15% equity from YPF and private partners.

The project reached financial close in early 2026 after demonstrating strong offtake agreements with international buyers.

Vaca Muerta Shale Field Infrastructure — Part of the massive development feeding the new Vaca Muerta Sur pipeline.

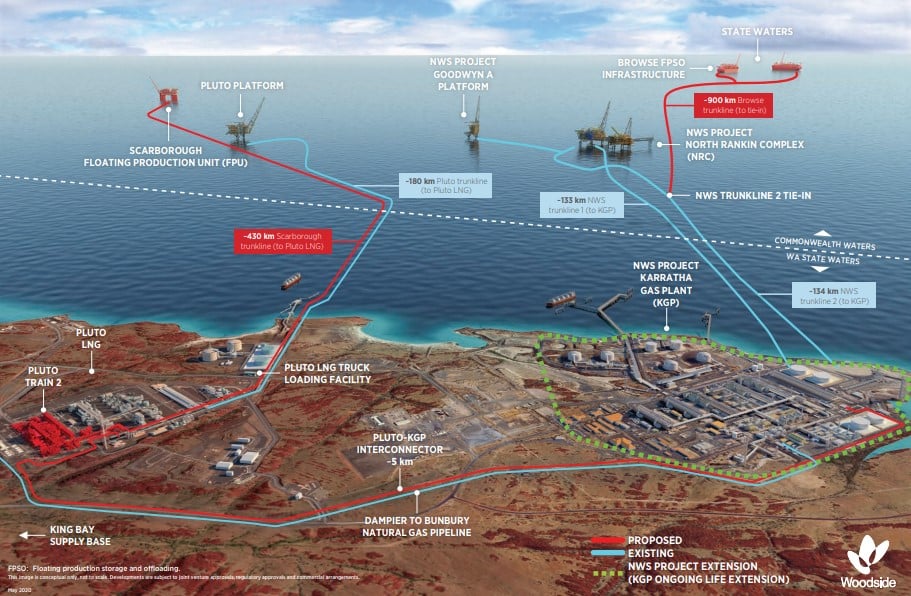

2. Australia – Scarborough Offshore Pipeline & Pluto Train 2

Woodside’s flagship project includes a 430 km subsea pipeline.

Financing:

- $5.5 billion total for the upstream and pipeline scope.

- Heavy use of sustainability-linked loans with margins tied to emissions reduction targets.

- Significant involvement from Japanese and Korean ECAs due to LNG offtake agreements.

Scarborough Floating Production Unit (FPU) and 430 km subsea pipeline — Artist’s rendering of the full development.

3. UK North Sea – Multiple CCUS-Linked Pipelines

Several North Sea operators are repurposing existing gas lines for CO₂ transport as part of the UK’s CCUS clusters.

These projects are attracting blended finance packages that include UK government grants, private equity, and green bonds — reducing the effective cost of capital by 150–200 basis points compared with pure commercial financing.

4. Gulf of Mexico – Subsea Tie-Back Projects (e.g., Beacon Shenandoah and others)

Smaller but high-return tie-backs are often financed through reserve-based lending (RBL) facilities, where the borrowing base is tied directly to proven reserves.

Offshore Pipeline Construction — Multi-billion-dollar mega-projects require sophisticated, blended financing structures in 2026.

What This Means for Subsea & Pipeline Professionals

The new financing reality creates both challenges and opportunities:

- Higher Scrutiny on ROI: Projects must now prove strong economics even at $70–$80/bbl oil prices.

- Demand for Technical Expertise: Lenders require detailed integrity assessments, digital twin models, and clear transition plans before releasing funds.

- New Career Paths: Engineers who understand project finance, ESG metrics, and cost modeling are increasingly valuable in business development and commercial roles.

Related Reading on Offshore Pipeline Insight:

- Maximizing Subsea Infrastructure Efficiency: Best Practices for 2026

- UK and Australia Petroleum Industry Outlook

- Innovations Driving Efficiency in Subsea Infrastructure

Outlook for the Rest of 2026 and Beyond

Analysts expect project finance activity to remain strong through 2027, especially for gas and energy transition pipelines. Private capital is flowing into the sector because offshore midstream assets offer stable, long-term cash flows with inflation-linked tariffs.The winners in 2026 will be operators and contractors who can present bankable projects with:

- Clear ESG credentials

- Robust technical risk mitigation (digital twins, robotics, advanced materials)

- Diversified revenue streams (hydrocarbons + CCUS/hydrogen)

Conclusion

Project financing for 2026 offshore pipeline mega-projects has evolved into a sophisticated blend of traditional debt, private equity, ECAs, and green finance instruments. The era of simple bank loans for new pipelines is largely over — success now depends on technical excellence, clear transition strategies, and creative structuring.

For subsea and pipeline engineers, understanding these financing realities is no longer optional. It directly affects which projects move forward, how quickly they are built, and what technologies get deployed.The steel and technology being financed today will define the offshore energy system for the next 30–40 years.

Written by Oko

Founder, Offshore Pipeline Insight

May 30, 2026.